Many beginners try budgeting for the first time and feel frustrated when it doesn’t work the way they expected. This isn’t because people are bad with money or lack discipline — it’s because real financial life in the United States is more dynamic than a simple spreadsheet or budgeting app can capture.

Most budgets are built on static numbers, while actual living costs shift week to week. Rent, Groceries, Transportation, Healthcare, and Subscriptions fluctuate throughout the year. Income isn’t always predictable either. Many US workers are paid biweekly, weekly, tip-based, or irregularly, which makes matching income to bills feel like a puzzle.

When beginners discover that budgeting doesn’t immediately produce control or clarity, they assume the budget failed — or that they failed the budget. In reality, budgeting starts with visibility, not perfection, and visibility takes time to form.

Why Budgeting Feels Hard for Beginners in the US

For many beginners, budgeting feels harder than expected because financial life in the United States is built around moving parts that don’t always fit neatly into categories. Most people weren’t taught how to track spending, plan for irregular bills, or forecast future expenses, so they enter adulthood learning through trial and error.

Another challenge is that income and expenses don’t operate on the same schedule. Many US workers are paid biweekly, weekly, or in variable amounts, while rent, insurance, and utilities are billed monthly. Trying to align those cash flows can feel confusing without a financial buffer or visibility into patterns.

Add rising living costs, subscription-based services, and healthcare variability, and budgeting becomes less about simple math and more about navigating a system with inconsistent timing and fluctuating demands.

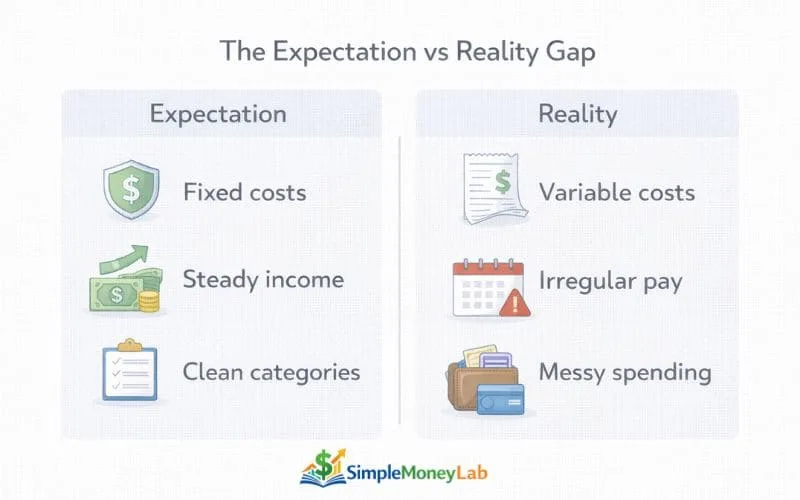

The Expectation vs Reality Gap

Many beginners believe budgeting will deliver instant control, predictability, and structure. The expectation is that once numbers are written down, money will begin to follow those numbers. In reality, life doesn’t always cooperate with static plans, especially in the US where core costs keep moving and income timing isn’t always uniform.

This gap between budgeting expectations and how financial life actually behaves creates early frustration — not because people are doing budgeting “wrong,” but because budgeting was never designed to track a perfectly stable world.

Static Budgets vs Dynamic Life Costs 🔄

Traditional budgets assume fixed numbers, yet real costs fluctuate. Rent increases annually, grocery prices shift week to week, gas changes based on market conditions, and healthcare can vary unpredictably. Subscriptions and seasonal expenses add more volatility. A static monthly sheet struggles to map onto a moving cost environment.

Irregular Pay Cycles vs Monthly Bills 💸

Many US workers are paid biweekly, weekly, or through variable income such as tips, gigs, or shift differentials. Meanwhile, major expenses like rent, utilities, insurance, and loan payments are due monthly. When deposits and withdrawals follow different rhythms, beginners feel like they’re always trying to catch the next cycle rather than planning ahead.

Variable Expenses vs App Categorization 🧩

Budgeting apps categorize transactions neatly, but real spending rarely fits into clean buckets. Grocery runs include household supplies, pharmacy items, or snacks. Transportation includes parking, tolls, maintenance, and fuel. Apps improve visibility, but they simplify the representation, not the underlying complexity. The messy part still belongs to the user.

Psychological Components of Budget Failure

Budgeting seems like a math exercise on the surface, but much of budgeting difficulty comes from behavioral and emotional patterns, not numerical limitations. When beginners feel like they “failed” budgeting, it’s often because human psychology wasn’t accounted for in the plan. Money touches stress, comfort, identity, and daily convenience — all of which shape spending more than formulas do.

Present Bias & Immediate Rewards 🎯

Human brains are wired to favor immediate rewards over long-term outcomes. Buying food delivery, getting a ride-share, or upgrading a service feels rewarding now, while budgeting benefits feel distant and abstract. This creates friction between the budget’s long-term planning horizon and the brain’s preference for short-term dopamine.

Budget Fatigue & Decision Overload 🧠

Modern financial life includes a constant stream of decisions: groceries, insurance, transportation, subscriptions, phone plans, utilities, medical expenses, and more. Beginners often assume budgeting will reduce decisions, but it can temporarily increase them as visibility improves. Too many financial choices without sufficient clarity leads to fatigue, which eventually results in avoidance.

Money Shame & Avoidance 🙈

When people feel behind financially, they often avoid looking at the numbers to reduce discomfort. Avoidance reduces stress in the moment, but removes the visibility budgeting requires. This pattern is common among US beginners and is also highlighted within Beginner Money Mistakes, where emotional discomfort influences financial habits more than knowledge gaps.

📍 Key Idea: Budgets fail when they don’t account for how people naturally cope with stress, uncertainty, and reward — not because beginners “lack discipline.”

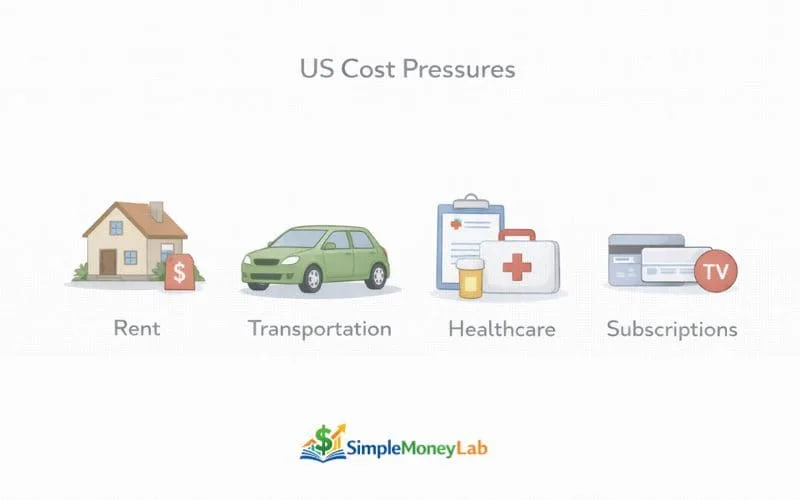

US-Specific Cost Pressures Beginners Face

Budgeting becomes harder when the core financial environment is expensive, unpredictable, and fragmented. Beginners in the United States encounter a set of structural cost pressures that make budgeting feel less like a planning exercise and more like a balancing act. These pressures don’t disappear with discipline or better math — they exist at the system level and shape how people allocate money month to month.

These are four major cost categories that often strain beginner budgets.

Housing & Rent Inflation 🏠

Housing is one of the largest expenses for young adults, and rent has increased across many cities faster than wages. Move-in costs, application fees, deposits, and required insurance amplify pressure during transitions. Because rent consumes such a large portion of income, beginners have less flexibility for other categories, making budgets easier to break.

Transportation & Car Costs 🚗

In most US cities, daily life depends on transportation. Car ownership includes fuel, parking, maintenance, registration, insurance, and repairs. Even public transportation involves monthly passes and unpredictable add-ons. These costs rarely stay consistent, and surprise repairs introduce volatility that budgets struggle to absorb.

Healthcare & Insurance Costs 🏥

Healthcare in the US introduces financial uncertainty through premiums, deductibles, copays, and out-of-network charges. Beginners often underestimate medical expenses when building a budget because costs do not appear every month. When they do appear, they can be large, disrupting the budgeting process and increasing stress around money management.

Subscriptions & Convenience Services 📱

Streaming platforms, delivery apps, cloud storage, fitness services, and software subscriptions have turned into recurring micro-expenses. While individually small, they accumulate over time and quietly raise the monthly baseline. Convenience services reduce time and effort, which makes them psychologically sticky — but they also challenge spending visibility for beginners.

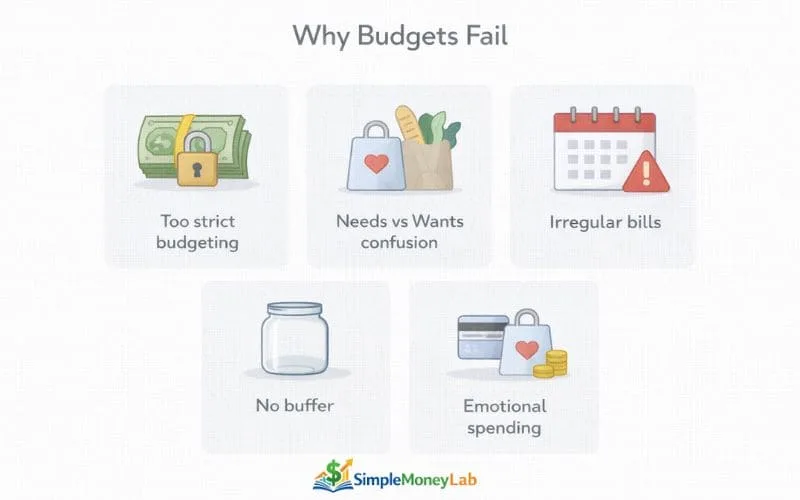

Beginner Budgeting Mistakes That Lead to Failure

Many budgets fail not because the idea of budgeting is flawed, but because beginners start with assumptions that don’t match real life. These common mistakes quietly increase friction, making budgeting feel exhausting instead of supportive.

Starting Too Strict 🚫

Beginners often create budgets that leave no room for flexibility. Every dollar is assigned, spending limits are tight, and small deviations feel like failure. This all-or-nothing approach works briefly, but collapses when real life introduces an unexpected expense or social obligation. Once the budget breaks, many people abandon it entirely rather than adjust it.

Confusing Needs vs Wants 🧠

Another common mistake is mislabeling expenses. Essentials and lifestyle choices often overlap, especially in a convenience-driven economy. Food delivery, Upgraded Phone plans, and Streaming services blur categories. Without clarity, spending feels unpredictable and guilt-driven. Learning Categorizing Needs vs Wants helps beginners reduce confusion without cutting enjoyment entirely.

Ignoring Annual or Irregular Bills 📅

Many beginners budget only for monthly expenses and forget about costs that show up once or twice a year. Car registration, Medical visits, Holidays, Travel, Gifts, and Home or Vehicle repairs don’t appear every month, but they still count. When these expenses arrive, they feel like emergencies — even though they were predictable.

No Emergency Buffer 🛟

Without a financial buffer, any surprise expense immediately disrupts the budget. This turns budgeting into a reactive cycle rather than a planning tool. Even a small cushion can reduce stress and prevent short-term decisions from undoing progress. A guide on Emergency funds explains why buffers matter more than perfect categories.

Budgets fail fastest when they ignore flexibility, human behavior, and time-based expenses.

One reason budgeting feels frustrating is that not all expenses behave the same way. Treating flexible costs like fixed ones often creates gaps. This is explained clearly in fixed vs variable expenses, where expense behavior is broken down for beginners.

Why Apps Don’t Automatically Fix Budgeting

Budgeting apps can make money easier to see, but they don’t make money easier to manage. Many beginners in the US download an app expecting immediate control over spending. When that control doesn’t appear, frustration sets in.

The gap isn’t the app.

The gap is between Visibility and Behavior.

Apps handle numbers well.

People handle emotions, habits, and trade-offs.

UI Simplifies Data but Not Behavior 📊

Apps are designed to organize information, not change behavior.

They can:

- Categorize transactions

- Show charts and trends

- Highlight totals

But they can’t:

- Reduce stress-driven spending

- Remove convenience temptations

- Change how people respond to fatigue or time pressure

Spending decisions still happen in real life, not inside the app.

Beginners Expect Control, Not Visibility 🔍

Many beginners assume budgeting will feel empowering right away.

Instead, it often feels uncomfortable.

Why?

- Spending patterns become visible

- Habits don’t match expectations

- Trade-offs feel more real

Budgets don’t create control first.

They create awareness first — and awareness can feel discouraging before it feels useful.

Tool Reliance vs Skill Building 🧱

Tools can support budgeting, but they don’t replace understanding.

Skills that matter more than tools:

- Recognizing spending patterns

- Planning for irregular expenses

- Separating guilt from awareness

- Adjusting expectations over time

When skills improve, tools feel easier to use.

When skills are missing, tools feel overwhelming.

Budgeting works best when tools support understanding — not when they’re expected to create it.

How Beginners Can Make Budgeting Work For Them

Budgeting doesn’t have to feel like a full reset or a personality change. For most beginners in the US, budgeting starts working when expectations shift away from perfection and toward understanding. Small adjustments in how money is viewed often matter more than strict rules.

These behavioral shifts help budgeting feel more realistic over time.

Visibility Comes Before Control 👀

Seeing where money actually goes is often the first turning point.

- Expenses feel less abstract

- Patterns become easier to notice

- Surprises feel less frequent

This stage can feel uncomfortable, but visibility is how budgeting begins to feel useful rather than restrictive.

Flexibility Reduces Burnout 🔄

Budgets break when they leave no room for real life.

- Costs change month to month

- Social spending is unpredictable

- Unexpected bills still happen

Flexibility allows a budget to adjust without feeling like failure.

Categorization Comfort Matters 🧩

Budgeting improves when categories feel realistic instead of perfect.

- Some expenses overlap

- Convenience blurs lines

- Not every purchase fits neatly

Learning Monthly Budgeting basics helps beginners create categories that reflect real spending, not ideal behavior.

A Buffer Mindset Lowers Stress 🛟

Budgets feel fragile without breathing room.

- Small cushions reduce urgency

- Surprises feel manageable

- Planning feels less reactive

A buffer doesn’t remove uncertainty, but it softens its impact.

Anti-Shame Framing Builds Consistency 🤍

Budgeting fails fastest when guilt takes over.

- Shame leads to avoidance

- Avoidance reduces visibility

- Reduced visibility increases stress

When budgeting is framed as learning rather than judging, consistency becomes easier to maintain.

Budgeting works best when it adapts to people — not when people are forced to adapt to it.

FAQs : Why Budgets Fail for Beginners (US)

Why do budgets fail for beginners?

Budgets often fail because they’re built around ideal behavior instead of real life. Beginners usually underestimate variable costs, irregular income timing, and emotional spending triggers. When a budget doesn’t match how money actually moves, it feels frustrating and gets abandoned — even though the problem isn’t the person.

Are budgets supposed to be strict?

No. Strict budgets tend to break faster, especially for beginners. In practice, budgets work better as flexible frameworks that help people understand patterns rather than control every dollar. When budgets are treated as learning tools instead of rules, they become easier to stick with.

Why does budgeting feel overwhelming?

Budgeting brings visibility to spending that was previously automatic. Seeing numbers clearly can feel uncomfortable at first, especially when costs fluctuate or don’t match expectations. The overwhelm usually comes from information overload, not from budgeting being inherently difficult.

Do budgeting apps make budgeting easier?

Budgeting apps can improve visibility, but they don’t remove emotional or behavioral challenges. Apps organize data well, but people still make decisions in real life under stress, time pressure, and convenience. For many beginners, apps feel helpful only after spending patterns become familiar.

How long until budgeting feels natural?

Budgeting typically feels more comfortable after several months of consistent visibility. As spending patterns repeat, surprises become less frequent and decision fatigue decreases. There’s no fixed timeline — comfort grows as familiarity replaces uncertainty.

Final Thoughts

Struggling with budgeting doesn’t mean someone is bad with money. For most beginners in the United States, budgeting feels difficult because it’s a skill learned in real time, not a habit taught early in life. Cost pressures, irregular income, and emotional spending all make the learning curve steeper.

Budgeting isn’t a personality trait. It’s not about being naturally disciplined or organized. It’s a process of building awareness, adjusting expectations, and becoming more comfortable with how money actually moves. When that shift happens, budgeting stops feeling like a test and starts feeling like a tool.

After recognizing why budgets fail, the next step is often improving spending visibility. Learning how to track spending without feeling overwhelmed helps beginners move from frustration to clarity without pressure or shame.

Budgeting improves when understanding replaces judgment.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.