Income terms can feel confusing for many beginners, especially when paychecks don’t match what people expect to take home. In the United States, earnings move through taxes, payroll deductions, and benefits before they become usable income. Because of this, many people aren’t sure what money is actually available for spending after essential deductions are taken out.

Understanding what is disposable income helps close this visibility gap. Disposable income is often confused with take-home pay or extra money, but it represents something more specific — income that remains after required taxes are removed. That distinction matters when thinking about spending, saving, and everyday financial flexibility.

Without clarity around income types, budgeting and spending decisions can feel unpredictable. When income is clearly understood, financial planning becomes easier to interpret and less stressful to manage.

Why Income Terms Feel Confusing in the US

Income can feel confusing because most people don’t interact with their full earnings directly. Instead, money moves through multiple deduction layers before it reaches a bank account. When different income labels are used to describe different stages of this process, it becomes harder to understand what each term actually means.

For many beginners, the confusion comes from seeing multiple income numbers without knowing how they connect to each other.

Common sources of confusion include:

- Gross vs Net vs Disposable income — Multiple income stages with different meanings

- Payroll deductions — Retirement contributions, Insurance premiums, and other employer-based deductions

- Tax withholding — Federal, State, and sometimes local taxes removed before payment is received

- Benefit deductions — Healthcare, Vision, Dental, and other benefit-related costs

Because these deductions happen automatically, many beginners only focus on their final deposit amount. Without understanding how income changes at each stage, it becomes harder to interpret how much money is actually available for everyday use.

Income confusion usually comes from layered deductions — Not from complicated math.

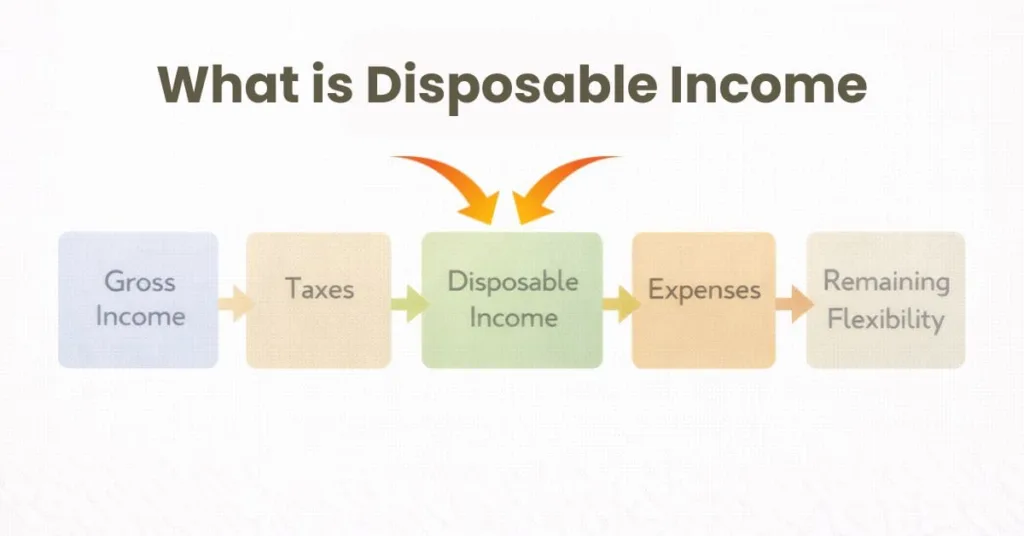

What Is Disposable Income?

Disposable income is the amount of money a person has available after required taxes are taken out of their earnings. It represents income that can be used for everyday living expenses, savings, or other financial priorities.

In simple terms, disposable income is what remains after the government-required portion of income is removed.

Real-Life Meaning

In real life, disposable income is the money people use to:

- Pay Rent and Utilities

- Buy Groceries and Daily Necessities

- Cover Transportation Costs

- Support Savings or Financial Goals

It is not extra income — It is usable income.

Disposable ≠ Free Money

Disposable income is often misunderstood as “extra” or optional money.

In reality:

- It still needs to cover essential expenses

- It includes money needed for variable monthly costs

- It reflects financial flexibility, not financial surplus

Understanding disposable income helps create clearer expectations about spending and planning. This is why learning Monthly Budgeting basics becomes easier once income stages are understood, since budgeting decisions depend on knowing what money is actually available after taxes.

Disposable income shows usable income — Not spare income.

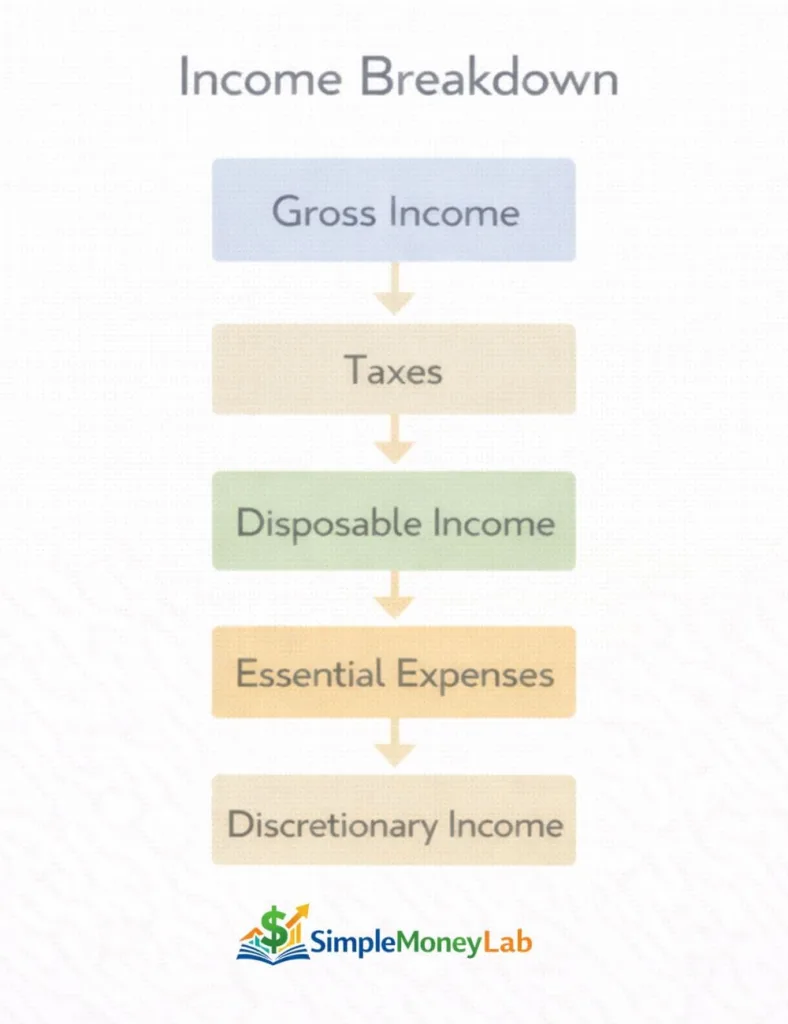

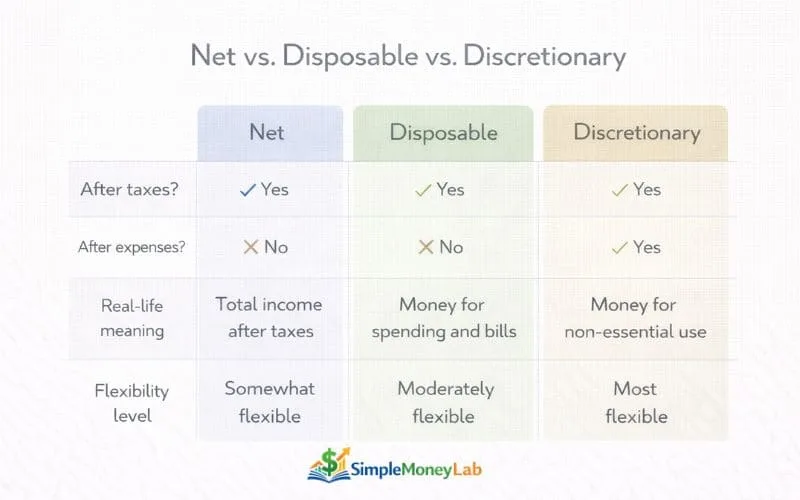

Disposable Income vs Net Income

Net income is the amount of money a person receives after taxes and most payroll deductions are removed. This is typically the number people see deposited into their bank account from their employer.

For many employees, Net income already reflects taxes, Insurance Premiums, Retirement contributions, and other paycheck deductions.

Disposable Income Difference

Disposable income focuses specifically on income remaining after required taxes are removed. It does not always account for voluntary payroll deductions like retirement contributions or certain benefit elections.

Because of this:

- Net income often reflects actual take-home deposit

- Disposable income reflects income after mandatory taxes only

- Disposable income is often used for economic measurement and financial analysis

Why People Mix Them

Many beginners use these terms interchangeably because both numbers appear smaller than gross income and relate to money available after deductions.

Confusion happens because:

- Paycheck statements show multiple income figures

- Deduction types are not always clearly labeled

- Real-life usage varies between finance education and economic data

Net income reflects what reaches your account, while disposable income reflects income remaining after required taxes.

Disposable Income vs Discretionary Income

Disposable income and Discretionary income sound similar, but they describe different stages of money availability.

Disposable income is money left After required taxes are removed.

Discretionary income is money left After taxes AND essential living expenses are paid.

In simple terms:

- Disposable income = Income available to spend

- Discretionary income = Income available after essentials are covered

This difference explains why someone can have disposable income but still feel financially tight.

Essential Expenses Role

Essential expenses are what separate disposable income from discretionary income.

These often include:

- Housing (Rent or Mortgage)

- Utilities

- Groceries

- Insurance

- Basic Transportation

- Minimum Debt Payments

Once these are covered, the remaining amount becomes discretionary income.

Real-World Example

Imagine a monthly income scenario:

After taxes → $3,500 = Disposable income

After rent, groceries, utilities, insurance → $600 = Discretionary income

This shows how disposable income measures usable income broadly, while discretionary income reflects optional spending flexibility.

Disposable income measures post-tax income, while discretionary income measures post-expense flexibility.

Why Disposable Income Matters in Everyday Financial Life

Disposable income influences how flexible daily financial decisions feel. When people understand how much income remains after taxes, spending patterns become easier to interpret and financial planning feels more predictable. Without this clarity, income and spending often feel disconnected.

Disposable income doesn’t just describe money — it helps explain financial comfort and stability.

Spending Flexibility 💳

Disposable income determines how much room exists for everyday choices.

- Daily Spending decisions

- Lifestyle flexibility

- Ability to Absorb Small cost increases

When disposable income is tight, even normal price changes can feel stressful.

Savings Potential 🏦

Disposable income also influences how easily savings can happen.

- Small Savings contributions

- Emergency preparation

- Long-term financial comfort

Higher disposable income usually creates more saving capacity, but even smaller disposable amounts can support gradual savings habits.

Debt Comfort 📉

Disposable income affects how manageable debt payments feel.

- Minimum payments feel easier to maintain

- Extra payments feel less stressful

- Unexpected expenses feel less disruptive

Lower disposable income can make fixed financial commitments feel heavier.

Stress Reduction 🧠

When disposable income is clearly understood, financial stress often decreases.

- Spending decisions feel clearer

- Surprise totals feel less common

- Planning feels more realistic

That clarity improves when spending patterns are visible. Learning How to track spending without overwhelm supports understanding how disposable income is actually used in daily life.

Disposable income helps explain financial flexibility — Not just financial totals.

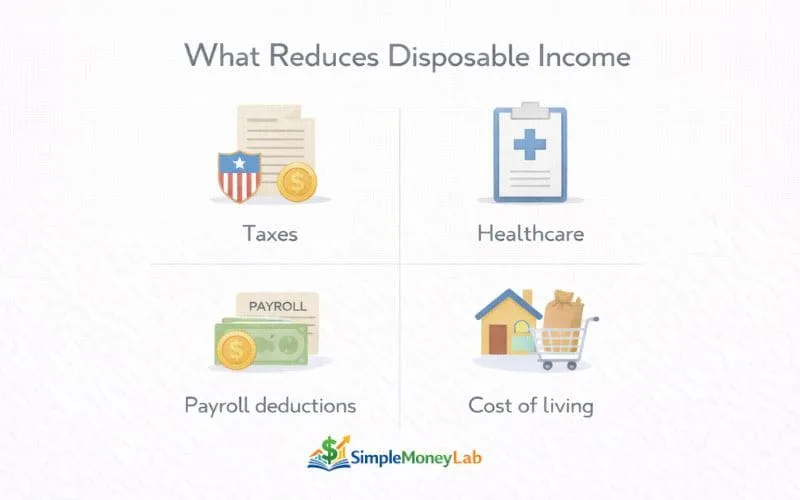

US-Specific Factors That Affect Disposable Income

Disposable income can vary widely in the United States because income doesn’t just depend on salary — It also depends on Taxes, Benefits, Deductions, and Regional Cost differences. Two people earning similar salaries can experience very different disposable income depending on these factors.

Understanding these structural differences helps explain why income can feel tighter or more flexible even at similar earning levels.

Taxes and Withholding 🧾

US income is affected by multiple tax layers.

- Federal Income tax

- State Income tax (in many states)

- Local taxes in some cities

- Payroll taxes for Social Security and Medicare

Withholding levels and tax structures can change how much income remains available after required deductions.

Healthcare Premiums 🏥

Healthcare costs can significantly affect usable income.

- Employer Health Insurance Premiums

- Dental and Vision add-ons

- Health Savings or Flexible spending contributions

These costs are often deducted directly from paychecks, reducing take-home income.

Cost of Living Differences 🏙️

Disposable income is strongly influenced by location.

- Housing costs vary widely by city

- Transportation costs differ by region

- Insurance costs vary by state

- Grocery and Service prices vary locally

Two identical salaries can create very different disposable income realities depending on location.

Payroll Deductions 📊

Beyond taxes and healthcare, payroll deductions can reduce available income.

- Retirement contributions

- Benefit programs

- Union or Membership dues

- Employer-Sponsored Savings programs

These deductions are often automatic, which can make income feel lower than expected if they aren’t clearly understood.

Disposable income in the US is shaped by systems, not just salary.

Common Beginner Misunderstandings About Disposable Income

Many beginners misunderstand disposable income because it sounds like money that can be spent freely. In reality, disposable income is still responsible for covering everyday living costs. When these misunderstandings happen, budgeting and spending expectations can become unrealistic.

Understanding what disposable income is not helps build more accurate financial awareness.

Disposable = Extra Money Myth 💰

One of the most common misconceptions is that disposable income means leftover or bonus money.

In reality:

- It still covers essential living costs

- It includes money needed for variable expenses

- It represents usable income, not spare income

Thinking of disposable income as “extra” often creates overspending expectations.

Ignoring Taxes 🧾

Some beginners think income becomes usable immediately after earning it.

In reality:

- Required taxes are removed first

- Tax withholding can vary by paycheck

- Tax changes can affect usable income mid-year

Not accounting for taxes can make income feel inconsistent or confusing.

Ignoring Irregular Costs 📅

Irregular expenses are often forgotten when thinking about usable income.

Examples include:

- Annual Insurance adjustments

- Medical bills

- Seasonal spending

- Car repairs

- Travel or Holiday costs

Understanding expense behavior helps explain why disposable income can feel different month to month. This is why knowing Fixed vs Variable expenses helps beginners see how stable and changing costs interact with usable income.

Disposable income is usable income — But still connected to real-world expenses.

How Beginners Can Think About Disposable Income Without Overhauling

Disposable income doesn’t need to be calculated perfectly to be useful. For many beginners, progress comes from understanding general income patterns rather than tracking every deduction in detail. When disposable income is viewed as an awareness tool instead of a precision calculation, it becomes easier to interpret and apply to everyday financial decisions.

A behavior-first perspective helps reduce pressure and keeps income awareness realistic over time.

Behavior Framing That Keeps Income Awareness Manageable 🧠

Simple mindset shifts often make disposable income easier to understand and use:

- Clarity > Perfection — Understanding income stages matters more than exact calculation accuracy

- Awareness > Control — Seeing income flow matters more than predicting every number

- Trend > Single Month — Income patterns matter more than one paycheck

- Realistic Expectations > Ideal Math — Real income changes over time, not in perfect formulas

This approach helps beginners see income as a moving financial signal instead of a fixed number that must always match expectations.

Disposable income works best as an awareness signal, not a precision target.

FAQs About The Disposable Income

What is disposable income in simple terms?

Disposable income is the amount of money a person has available after required taxes are removed from their earnings. It represents income that can be used for everyday living expenses such as housing, groceries, transportation, and savings. It does not mean extra or bonus money — it means usable income after taxes.

Is disposable income after taxes?

Yes. Disposable income is calculated after mandatory taxes like federal income tax, payroll taxes, and applicable state or local taxes are deducted. It focuses on income remaining after required government deductions, not after all personal expenses.

Is disposable income the same as take-home pay?

Not always. Take-home pay usually reflects income after taxes and most payroll deductions, including benefits and retirement contributions. Disposable income focuses specifically on income remaining after required taxes, so the two numbers may be similar but are not always identical.

Why is disposable income important?

Disposable income helps explain how much financial flexibility someone has in everyday life. It influences spending comfort, saving potential, and how manageable fixed financial commitments feel. Understanding disposable income helps connect income levels with real-world spending and planning expectations.

How does disposable income affect budgeting?

Disposable income helps define how much money is realistically available to cover living costs and financial priorities. When disposable income is misunderstood, budgets can feel unrealistic or restrictive. When it is understood clearly, budgeting decisions often feel more grounded and predictable.

Can disposable income change monthly?

Yes. Disposable income can change if taxes, deductions, work hours, bonuses, or benefit costs change. It can also feel different depending on seasonal expenses, healthcare costs, or changes in payroll deductions. Because of this, disposable income is often better understood as a pattern over time rather than a fixed number.

Final Thoughts

Confusion around income terms is normal, especially when multiple paycheck numbers exist and deductions happen automatically. Most beginners are never formally taught how income flows from gross pay to usable income. Learning these concepts is a process, not something people are expected to know automatically.

Understanding disposable income helps connect earnings to real-life financial flexibility. When income is clearly understood, spending and saving decisions feel more grounded and predictable. Clarity often builds confidence over time, because financial behavior becomes easier to interpret.

Disposable income also helps explain how financial buffers are built gradually. Learning Emergency Fund basics helps show how usable income can slowly support financial stability and protection from unexpected costs.

Income clarity builds financial confidence through understanding, not perfection.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.