Many beginners feel anxious when checking their credit scores, especially when the number does not change as quickly as expected. It can be confusing to see a payment made or a balance reduced, yet the score appears unchanged for days or even weeks. This creates a gap between financial action and visible results.

Understanding how often do credit scores update helps explain why score changes do not always happen instantly. Credit scores are recalculated based on information reported by lenders, and that reporting follows specific timelines inside the US credit system.

Because the United States relies on multiple credit bureaus and structured reporting cycles, score updates depend on when account activity is reported and processed. Credit scores reflect reporting patterns over time rather than real-time financial activity.

Why Credit Score Updates Feel Confusing

For many beginners, credit scores feel like live numbers that should move immediately after every payment or balance change. When the score stays the same, it can create uncertainty or frustration. The confusion usually comes from misunderstanding how credit reporting and score recalculation actually work.

Credit systems are structured around reporting cycles, not real-time activity.

📱 Score Monitoring Anxiety

Many people now check their credit scores through apps or online dashboards. Because these platforms are easy to access, it can feel like scores should update instantly.

This can create:

- Expectation of daily movement

- Stress when numbers don’t change

- Confusion after making payments

Credit scores are not designed to function like stock prices.

🔄 App Refresh Misunderstanding

Refreshing a credit monitoring app does not trigger a new score calculation.

Apps display the most recently calculated score based on the latest reported data. If no new account information has been reported to credit bureaus, the score usually remains the same.

Score updates depend on reporting activity, not app refresh activity.

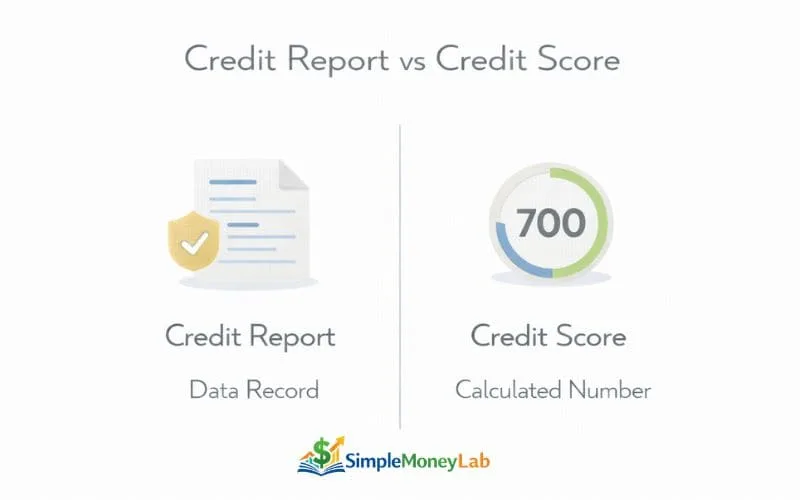

📄 Credit Report vs Credit Score Difference

Another common confusion is mixing up credit reports and credit scores.

- Credit report = Detailed record of account activity

- Credit score = Numerical summary based on report data

A credit report may update when lenders send new information, and a credit score is recalculated after that updated information is processed.

The two are connected but not identical.

US Multi-Bureau System

In the United States, there are multiple credit bureaus, and lenders may report to one, two, or all of them.

This means:

- Scores can differ across bureaus

- Update timing can vary

- Reporting cycles are not always synchronized

Because of this multi-bureau structure, credit score updates may not happen at the same time across all platforms.

Credit score updates feel confusing because they depend on reporting cycles and bureau systems, not real-time financial actions.

How Often Do Credit Scores Update?

Credit scores update when new information is reported to credit bureaus and processed into the credit report. In most cases, this happens on a recurring reporting cycle rather than in real time.

For many US consumers, credit card issuers and lenders typically report account activity on a monthly basis. When new account data is reported, credit scores are recalculated based on the updated information.

Credit scores do not automatically update every day — they update when reported data changes.

🧾 Real-Life Meaning

In real life, this means credit score changes usually follow reporting cycles.

For example:

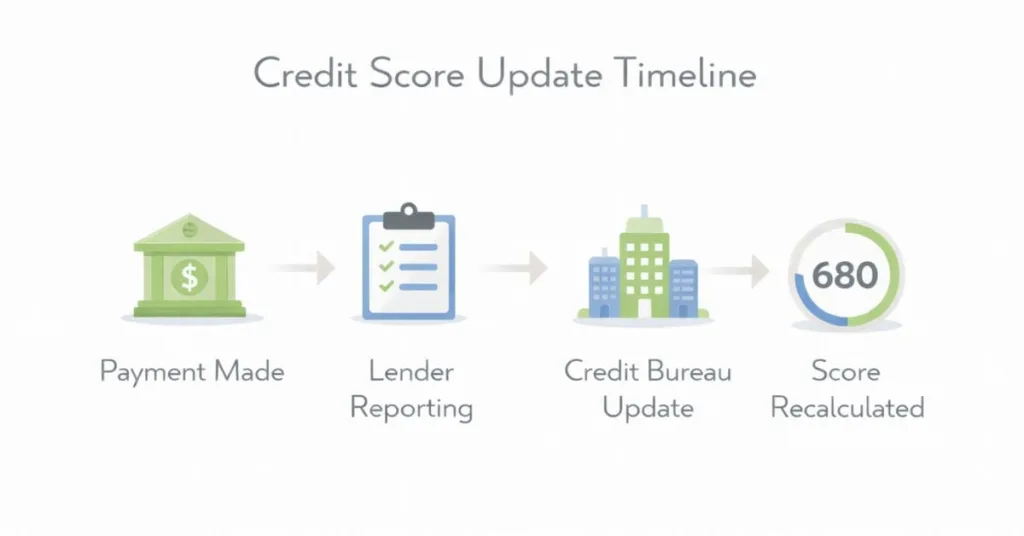

- A payment is made

- The lender reports updated balance data

- The credit bureau updates the report

- The score is recalculated

If no new activity is reported, the score may remain unchanged even if financial behavior has improved.

Understanding how reporting timelines work also connects to learning Why Payment History Matters, since payment data becomes part of the information that triggers score recalculations.

🔄 Credit Score ≠ Credit Report Timing

Another common misunderstanding is assuming that credit reports and credit scores update at the same exact moment.

In reality:

- Lenders send data on reporting schedules

- Credit reports update when new data is processed

- Credit scores update after report changes are reflected

Because of this sequence, there can be a delay between financial action and visible score movement.

Credit scores update after lenders report new account data — not instantly after payments are made.

What Triggers Credit Score Updates in the US

Credit scores update when new account information is reported and processed into a credit report. Score changes are not random — they are usually triggered by specific types of account activity that lenders send to credit bureaus.

Understanding what causes updates can reduce confusion about why scores move — or don’t move — after financial actions.

💳 New Reported Balance

When a lender reports an updated credit card balance, the new balance becomes part of the credit report.

This can affect:

- Credit utilization percentage

- Total outstanding balances

- Available credit levels

Because credit utilization is calculated using reported balances, learning what is credit utilization helps explain why balance updates can trigger score recalculations.

✅ Payment Reporting

When payments are reported as on time or late, that information becomes part of payment history data.

Payment reporting can:

- Strengthen positive payment patterns

- Reflect missed payment status

- Update account standing

Since payment history is one of the strongest credit factors, new payment data can influence score updates.

🆕 New Account Activity

Opening or closing an account may trigger credit report updates.

New account activity can affect:

- Credit age

- Credit mix

- Available credit totals

Changes in account structure can lead to score recalculations once reported.

🔍 Hard Inquiries

When a lender checks credit for an application, a hard inquiry may be recorded.

Hard inquiries can:

- Appear on credit reports

- Become part of credit activity records

- Factor into credit score models

Once reported, inquiry activity can trigger a score update.

📈 Credit Limit Changes

If a lender increases or decreases a credit limit, that change affects available credit.

Limit changes can influence:

- Overall credit utilization ratio

- Total credit capacity

- Balance-to-limit comparisons

Since utilization depends on both balance and limit, reported limit changes can cause score recalculations.

Credit score updates are triggered by new reported account data — not simply by checking a credit score app.

Credit Score vs Credit Report Updates

Many beginners assume that a credit report and a credit score update at the same time. In reality, they are connected but separate parts of the credit system. Understanding the difference helps explain why scores sometimes stay unchanged even after financial activity.

A credit report is the data record. A credit score is a calculation based on that data.

📄 Report Update Frequency

A credit report updates when lenders send new account information to credit bureaus.

This usually includes:

- Updated balances

- Payment status

- Account changes

- New inquiries

Reporting often follows monthly billing cycles, though timing can vary by lender.

If no new data is reported, the credit report does not change.

📊 Score Recalculation Timing

A credit score is recalculated after updated report data is processed.

This means:

- Report changes must happen first

- Score recalculation happens afterward

- Timing depends on when new data is received

Credit scores are generated using the latest available report information. Learning how credit scores work helps explain how score models use report data to calculate updated scores.

⏳ Why a Score May Not Move Instantly

A score may not change immediately for several reasons:

- The lender has not reported new data yet

- The reporting cycle has not closed

- The new data does not significantly change risk patterns

- Different bureaus updated at different times

Because of this structure, there can be a natural delay between taking financial action and seeing a score adjustment.

Credit reports update when lenders send new account information to credit bureaus, typically based on billing cycles rather than daily activity. The Federal Trade Commission explains through its credit report update guidance that lenders report account information periodically, which is why changes may not appear immediately after a payment or balance adjustment.

Credit reports update when lenders send new data, and credit scores update only after that new data is processed.

Why Credit Scores Don’t Update Daily

Many beginners expect credit scores to behave like live financial dashboards. In reality, credit scores are tied to reporting systems that operate on scheduled cycles rather than real-time activity.

Credit systems are built around structured data updates, not continuous recalculation.

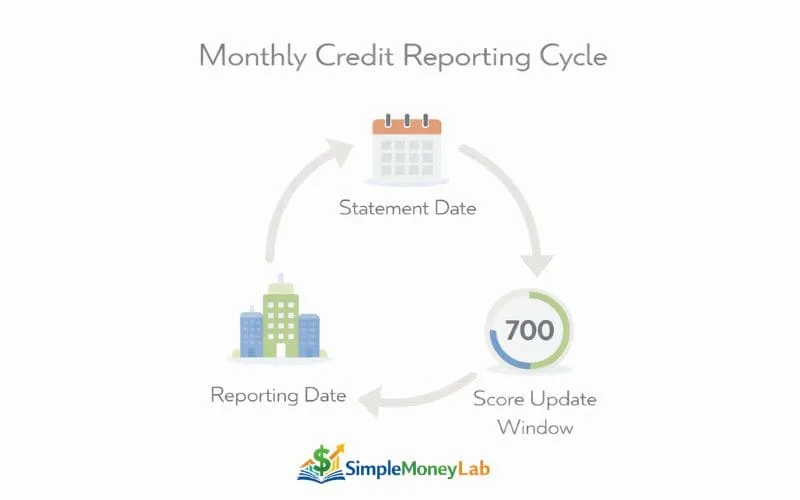

📅 Reporting Cycles

Most lenders report account activity on recurring billing cycles, often aligned with statement closing dates.

This means:

- Balances are reported after statement periods

- Payment status updates follow reporting schedules

- Score changes depend on reported data timing

If no new data is reported, the score typically stays the same.

🏦 Lender Batch Updates

Lenders often send account updates in batches rather than instantly after every transaction.

This can include:

- Grouped account updates

- Scheduled reporting windows

- Periodic balance and Status updates

Because reporting is batched, daily financial activity does not automatically trigger daily score changes.

🔄 System Recalculation Timing

Credit scores are calculated based on the most recently processed credit report data.

Score recalculations happen when:

- New account information is processed

- Report data changes

- Scoring models generate updated outputs

Without new processed data, recalculation does not occur.

Multi-Bureau Variation

In the United States, multiple credit bureaus operate independently.

This means:

- Lenders may report to one bureau before another

- Update timing may vary

- Score versions can differ slightly

Because of this structure, credit scores may update at different times depending on the bureau and reporting cycle.

Credit scores don’t update daily because they depend on scheduled reporting cycles and processed account data — not real-time transactions.

US Credit Reporting Timeline Explained

Credit score updates are closely connected to how and when lenders report account information. In the United States, reporting usually follows structured monthly billing cycles rather than real-time activity. Understanding this timeline helps explain why credit scores often change in predictable patterns rather than daily movements.

Credit reporting is built around account cycles, statement dates, and data processing windows.

📅 Monthly Reporting Pattern

Most credit card issuers and lenders report account information approximately once per billing cycle.

This typically includes:

- Updated balances

- Payment status

- Account standing

- Credit limit information

Because reporting usually happens monthly, credit score updates often follow a similar rhythm.

🧾 Statement Date Impact

Statement closing dates often influence when balances are reported.

This means:

- Balances at statement close may be reported

- Payment timing relative to the statement date can affect reported data

- Reported utilization reflects statement cycle data

Understanding statement timing helps explain why score changes may appear weeks after payments are made.

⏳ 30-Day Reporting Cycles

Many accounts follow reporting cycles that align with roughly 30-day billing periods.

These cycles help create:

- Structured update windows

- Predictable reporting intervals

- Periodic score recalculation opportunities

Score updates usually happen after these reporting windows close and new data is processed.

🔄 Dynamic Changes Over Time

Although reporting cycles are structured, credit data remains dynamic.

Score changes can occur when:

Balances fluctuate

Limits change

New accounts are reported

Payment status updates

Because of this, credit scores move in response to reported changes — but only after new data enters the reporting system.

In the US credit system, score updates typically follow monthly reporting cycles influenced by statement dates and processed account data.

Common Beginner Misunderstandings About Score Updates

Credit score updates often feel mysterious because expectations are shaped by apps, notifications, and quick digital feedback. In reality, credit reporting follows structured cycles that do not always align with everyday financial actions.

Many beginner misunderstandings come from expecting real-time changes in a system that operates on reporting schedules.

📱 “Credit Scores Update Every Day” Myth

Because credit monitoring apps are available 24/7, it can feel like scores should move daily.

In reality:

- Scores update after new data is reported

- No new report data = No recalculation

- Refreshing an app does not trigger updates

Credit scores are data-driven, not refresh-driven.

💳 “Paying Once Updates Instantly” Myth

Making a payment is important, but score updates depend on reporting timelines.

This means:

- Payment must be reported first

- Reporting happens on billing cycles

- Score recalculation happens after report processing

There can be a delay between financial action and visible score movement.

🏦 “All Bureaus Update at the Same Time” Myth

The US credit system operates with multiple independent credit bureaus.

This means:

- Lenders may report to bureaus at different times

- Updates may appear on one bureau before another

- Score versions may differ slightly

Because of this structure, score changes are not always synchronized.

Understanding broader financial behavior patterns helps reduce frustration around credit expectations. Learning about common beginner money mistakes helps connect credit misunderstandings to overall financial learning curves.

Most score update confusion comes from expecting instant changes in a system built around reporting cycles.

How Beginners Can Think About Credit Score Updates

For many beginners, credit score changes can feel urgent and emotional. When the number does not move quickly, it can create frustration or doubt. In reality, credit systems are designed to measure patterns over time, not instant financial reactions.

Understanding how reporting cycles work can help shift focus from short-term movement to long-term credit stability.

⏳ Timeline > Instant Results

Credit scores reflect reported data across billing cycles.

- Updates follow reporting schedules

- Changes appear after processing

- Improvement usually builds gradually

Credit systems reward long-term stability more than short-term adjustments.

📊 Pattern > Single Payment

One payment rarely defines overall credit behavior.

- Trends across months matter more

- Consistent reporting builds stronger signals

- Short-term fluctuations are common

Credit scores evaluate patterns, not isolated moments.

📅 Reporting Cycle Awareness

Knowing that lenders report on structured cycles helps reduce confusion.

- Statement dates influence reported balances

- Monthly reporting creates update windows

- Multi-bureau timing can vary

Understanding reporting timing improves realistic expectations.

🧘 Patience > Panic

Credit reporting systems are structured for long-term reliability measurement.

- Delayed updates are normal

- Gradual score movement is common

- Stability develops over time

Learning how credit builds over months and years helps create healthier expectations. Exploring how long it takes to build credit from zero helps connect score updates to broader credit development timelines.

Credit score updates follow reporting cycles and long-term behavior patterns, not instant financial actions.

FAQs

How often do credit scores update in the US?

Credit scores in the US typically update when new account information is reported to credit bureaus and processed. For many accounts, this happens on a monthly reporting cycle, though timing can vary by lender and bureau.

Scores do not update in real time — they update after new reported data changes the credit report.

Does a credit score update every month?

A credit score can update monthly if lenders report new account information during that billing cycle. However, if no new data is reported, the score may remain unchanged.

Score updates depend on reporting activity rather than a fixed monthly calendar date.

Why hasn’t my credit score updated yet?

A credit score may not update if:

The lender has not reported new data

The reporting cycle has not closed

The reported change does not significantly affect scoring factors

Credit score updates are tied to when account data is processed, not when payments are made.

How long after a payment does a credit score update?

A credit score usually updates after the lender reports the payment to credit bureaus and the updated data is processed. This often aligns with the account’s billing cycle rather than the exact payment date.

Because of reporting schedules, there can be a delay between payment and visible score change.

Do all credit bureaus update at the same time?

No. Credit bureaus operate independently, and lenders may report to them at different times.

This can result in:

Slight differences between bureau reports

Different update timing

Minor score variations across platforms

Can a credit score change daily?

A credit score can change whenever new reported data is processed, but daily changes are uncommon unless frequent account updates occur.

Most score changes follow reporting cycles rather than daily activity.

Final Thoughts

Watching credit scores too closely can create unnecessary stress, especially when numbers don’t move as quickly as expected. Most score updates follow reporting cycles, not daily activity, which means delays are normal inside the credit system.

Credit is not a real-time performance metric — it is a reporting cycle system. Scores change when new account data is reported and processed, not simply when financial actions happen. Understanding this structure helps reduce frustration and build more realistic expectations.

Over time, credit scores reflect long-term behavior patterns rather than single payments or short-term changes. As credit knowledge grows, it becomes easier to see score updates as part of a broader system rather than instant feedback.

Understanding how inquiries affect credit is often the next step in learning how score changes appear on credit reports. Exploring hard vs soft inquiry differences helps connect reporting activity to score movement patterns.

Credit growth usually follows reporting cycles — not refresh buttons.