Understanding credit can feel confusing when you’re just getting started. Many beginners hear about “credit scores” but aren’t sure what they mean or why they matter. In the United States, credit plays a big role in everyday financial life, and not knowing how it works can create a lot of stress or uncertainty. 💭

A credit score isn’t just a number for loans — it can affect practical things like renting an apartment, getting a cell phone plan, or qualifying for a credit card. Because of that, having at least a basic understanding of credit can make day-to-day decisions easier and less intimidating. 📍

This beginner guide explains what is a credit score, how it works, and why it matters, without overwhelming financial terminology. The goal is simple: to give you clarity and confidence about credit so you can make informed decisions moving forward.

What Is a Credit Score?

A credit score is a three-digit number that shows how likely you are to repay borrowed money. Lenders and financial institutions use it to evaluate your creditworthiness and the level of risk involved in lending to you. ✔️

In the United States, most credit scores fall between 300 and 850. A higher score generally suggests a lower risk to lenders, while a lower score indicates higher risk. Credit scores aren’t random — they’re calculated from the information in your credit report, which includes your past borrowing and repayment history.

Credit scores matter because they influence access to financial products such as credit cards, loans, and other forms of financing. Even if you’re not borrowing money today, your score can affect practical decisions later, making it useful to understand how the system works early on.

How Does a Credit Score Work?

A credit score is not created randomly — it’s calculated using the financial information in your credit report. To understand how a credit score works, it helps to look at two parts of the system: credit reporting and scoring models.

Credit Reporting 📋

Credit reporting begins with credit bureaus, which are organizations that collect financial information from lenders, banks, and other institutions. These details include things like payments, balances, credit usage, and account history.

The information is compiled into a credit report, which serves as a record of your past borrowing and repayment behavior. Your credit score is then calculated from this credit report, meaning the score reflects the data stored there rather than real-time transactions.

Credit scores are recalculated whenever new report data is processed. Understanding how often do credit scores update helps explain how scoring models respond to newly reported account activity.

Scoring Models 🧾

Once the credit report is created, credit scoring models are used to convert that information into a three-digit score. In the United States, two of the most widely used scoring models are:

- FICO

- VantageScore

Both scoring models use similar financial information, but they may weigh certain details differently. As a result, your credit score can vary slightly depending on which model is being used and which lender is reviewing it.

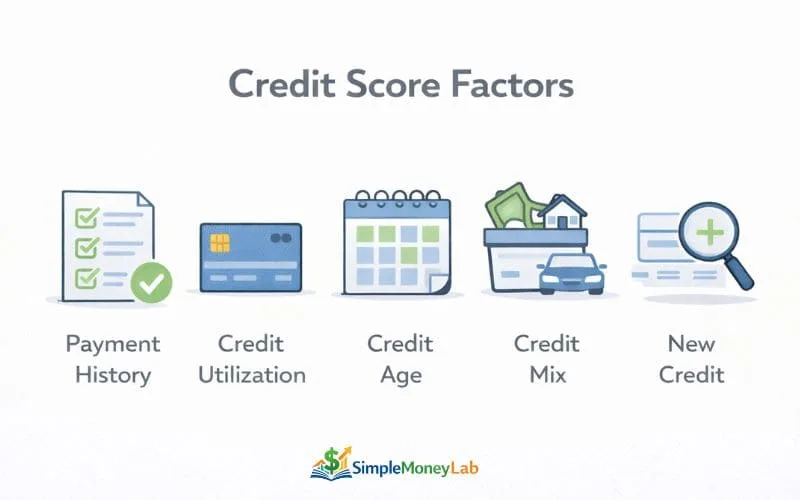

What Factors Affect Your Credit Score?

Credit scores are based on several key factors that reflect how you’ve managed credit in the past. While different scoring models may weigh these factors differently, the general categories remain similar across most systems in the United States. Here are the main areas that influence your score:

🧾 Payment History

Payment history shows whether you’ve made payments on time for credit cards, loans, and other accounts. Late or missed payments may signal risk to lenders, while a positive history can help build trust over time.

Credit scores are calculated using multiple behavior signals, and payment reliability is one of the most important factors in that evaluation. Understanding why payment history matters helps explain how consistent on-time payments influence overall credit score behavior.

💳 Credit Utilization

Credit utilization refers to how much of your available credit you’re currently using. Using a portion of your available credit is normal, but consistently using a large share of it may be viewed as higher risk by scoring models.

Credit scores are calculated using multiple credit behavior signals, and each factor helps show a different part of credit usage patterns. Understanding what is credit utilization helps explain how credit card usage levels influence overall credit behavior and scoring models.

📅 Credit Age

Credit age looks at how long your credit accounts have been open and active. A longer credit history provides more data for scoring models and can make your score more stable compared to a newer credit file.

📚 Credit Mix

Credit mix reflects the variety of credit accounts you’ve used, such as credit cards, auto loans, personal loans, or student loans. Scoring models consider this because managing different types of credit can help demonstrate financial responsibility.

🛠 New Credit

New credit includes recently opened accounts and recent credit inquiries. Opening several accounts in a short period of time may create extra risk signals for scoring models, especially if you’re new to credit.

Why Credit Scores Matter (US)

Credit scores affect more than just borrowing. In the United States, they play a role in many everyday financial decisions because they help companies understand how reliably a person has handled credit in the past. Even if you’re not planning to apply for a loan today, your credit score can influence opportunities and costs in other areas of life. Here are some common examples:

🏠 Renting an Apartment

Landlords and property managers often review credit to get a sense of payment reliability. A stronger credit profile may make the rental approval process smoother, while a limited or new credit history may require additional paperwork or verification.

📱 Cell Phone Plans

Some wireless carriers check credit before offering postpaid cell phone plans. If credit information is limited, carriers may request a deposit or recommend a prepaid plan instead.

🚗 Car Insurance

In certain states, auto insurers may use credit information as one factor when determining rates. This does not apply in every state, but it is a common practice in many parts of the country, especially for young drivers.

🔌 Utilities and Services

Utility companies for electricity, water, or internet services may check credit when opening a new account. If credit history is limited, some providers may ask for a small deposit as a standard precaution.

💳 Credit Card Approvals

Banks and credit card issuers use credit scores to evaluate applications and determine which products a customer qualifies for. Credit scores may also influence starting credit limits and terms offered.

🚘 Auto Loans & 🚸 Student Loans

For people financing a car or using private student loan options, credit information is commonly reviewed to assess eligibility. A stronger credit profile may result in more options to choose from, while limited history can narrow available choices.

Overall, credit scores matter because they help companies make decisions based on financial history rather than just income or personal information. Understanding how credit works early on can make financial transitions—like moving, studying, or starting out independently—feel more predictable and less stressful.

Understanding how scores are calculated is helpful, but beginners often wonder How Credit Scores affect your Financial life in practical terms.

Many beginners also wonder how long it takes to build credit from zero, since credit scores do not appear immediately for new credit users.

What Is Considered a “Good” Credit Score?

Most credit scores in the United States range from 300 to 850, with higher numbers generally viewed as less risky by lenders and financial institutions. While exact ranges can vary slightly depending on the scoring model, the table below shows a commonly used breakdown for FICO scores, which are widely referenced in the U.S. credit system for educational purposes:

| Credit Score Range | Category |

|---|---|

| 800–850 | Exceptional |

| 740–799 | Very Good |

| 670–739 | Good |

| 580–669 | Fair |

| Below 580 | Poor |

These categories are meant to give a general idea of how credit scores are viewed, not to set a required target for individuals. A person’s financial situation, goals, and timeline can influence how they approach credit, and credit scores naturally change over time as new information is added to credit reports.

Understanding where scores fall on the scale helps beginners see how credit fits into everyday financial decisions and why credit education can make transitions—like renting, applying for services, or moving out on your own—feel more manageable.

Credit Score vs Credit Report

Credit scores and credit reports are closely related, but they are not the same thing. This is one area where many beginners get confused, especially when checking their credit for the first time. Understanding the difference makes the entire credit system much easier to navigate.

A credit report is a detailed record of your borrowing and repayment history. It includes information such as credit card accounts, loan balances, payment history, credit usage, and account opening dates. In other words, the credit report contains the raw data that represents how you’ve managed credit over time.

A credit score, on the other hand, is a three-digit number calculated from the information in your credit report. Scoring models analyze the data in your report and convert it into a score that lenders can quickly interpret.

A simple way to think about it is:

Credit report = your credit data

Credit score = number calculated from that data

Both matter, but for different reasons. The report provides the full context, while the score offers a quick summary that lenders and companies can use when making decisions. If you’re new to credit, understanding what a credit report is will make it easier to understand how scores are created and why they change over time.

Common Credit Score Myths

Credit can feel more confusing than it really is, partly because there are many myths about how credit scores work. Clearing up these misunderstandings makes it easier for beginners to navigate the credit system with more confidence and less stress. Here are a few common myths:

❌ Myth: Credit Scores only Matter for loans

Many people assume credit scores are only checked when applying for loans. In reality, credit information may also be reviewed for renting an apartment, opening certain utility accounts, getting a cell phone plan, or applying for a credit card. In the U.S., credit is used in more everyday situations than most beginners expect.

❌ Myth: Checking your own Credit Score hurts your score

This is a common misunderstanding. When you check your own credit through a credit monitoring service or through a lender’s educational tool, it’s typically considered a soft inquiry, which does not impact your score. Soft inquiries are different from hard inquiries, which are used for credit applications and reviewed by scoring models differently.

❌ Myth: Income affects your Credit Score

Income can influence your financial situation, but it isn’t included in credit scoring models. Scoring models look at credit activity—such as payments, balances, and account history—rather than how much money a person earns. However, income can indirectly affect credit usage because it may influence how comfortably a person manages bills and debt.

Explaining these myths is helpful because credit can feel intimidating when information is unclear. Understanding how credit actually works makes the credit system more approachable for beginners and reduces the guesswork involved in everyday financial decisions.

Frequently Asked Questions

Does checking my credit score lower it?

No. Checking your own credit through a credit monitoring service or lender’s educational tool is considered a soft inquiry, which does not impact your credit score. Soft inquiries simply allow you to view your credit information without signaling a credit application. Hard inquiries, on the other hand, may appear when you apply for new credit, such as credit cards or loans, and are viewed differently by scoring models. Checking your score regularly can help you stay informed without affecting your credit.

What credit score do I start with?

Most people do not begin with a credit score at all. Credit scores are generated only after a person has used credit for a period of time and enough information has been reported to credit bureaus. The length of time needed can vary depending on the type of accounts used and how often lenders report data. Once a credit history becomes established, scoring models can calculate a score based on that information.

What is the highest possible credit score?

A common maximum score used by many scoring models is 850, although not everyone will reach that number, and it is not necessary to do so. Scores in the higher ranges generally indicate a lower level of risk to lenders, but the specific ranges and labels can vary slightly across scoring models. Credit scores naturally change over time as new information is added to your credit report.

Does rent affect my credit score?

Rent payments don’t automatically appear on credit reports the way credit card or loan payments do. However, some landlords and rental reporting services may choose to report rental payments, which can help build credit history. Reporting is not universal, so whether rent affects credit depends on how the data is handled by property managers and reporting companies. If rental data is not reported, it won’t influence credit scores directly.

Can I have a credit score with no credit history?

It’s possible not to have a credit score if there isn’t enough data for scoring models to analyze. This is sometimes called having a “thin credit file” or “no credit file.” People who are new to credit, including young adults and newcomers to the United States, commonly experience this situation. Building a credit history typically requires having at least one credit account that reports activity to the credit bureaus over time.

Final Thoughts on Credit Scores

Credit scores can seem complicated at first, especially if you’re just starting to learn how the credit system works in the United States. But like most financial topics, credit becomes more understandable once you break it down into smaller parts: how credit data is collected, how scoring models interpret that data, and how credit information fits into everyday decisions.

Progress with credit doesn’t need to be perfect. Scores naturally change over time based on financial activity, and everyone begins from a different starting point. The goal for beginners isn’t to chase a specific number — it’s to build awareness, stay informed, and make decisions with more clarity and less stress.

Understanding the basics of credit earlier in life can make future milestones — such as renting, financing, or accessing services — feel more predictable and less confusing. With time, credit becomes less of a mystery and more of a practical tool that supports your financial journey.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.