Many beginners are surprised to learn that not everyone has the same type of credit history. When reviewing credit reports or learning about credit scores, terms like thin file vs no file can create confusion, especially for people who are just starting to understand the US credit system.

A credit file is essentially a record of your credit activity. It includes information about accounts, payment history, and other data used by lenders to evaluate financial reliability. However, some individuals have very limited credit records, while others may not have a credit record at all.

Understanding the difference between thin file and no file helps explain how credit history develops and why some people have less information on their credit reports than others.

Why Credit History Matters

Credit history plays an important role in how financial institutions understand a person’s borrowing behavior. In the United States, credit reports serve as a record of how someone has used credit over time.

These records help create a clearer picture of financial reliability.

📄 Credit Reports Track History

A credit report collects information about credit-related activity across time.

This may include:

- Credit Accounts

- Payment Records

- Credit Limits

- Account History

Together, these details form the foundation of a credit profile that lenders can review when evaluating financial decisions.

🏦 Lenders Evaluate Reliability

Lenders often review credit history to understand how consistently someone has managed credit responsibilities in the past.

Credit reports may help lenders observe patterns such as:

- Repayment behavior

- Account management

- Overall Credit activity

This historical record helps lenders evaluate risk when considering new applications.

🔑 Credit Access Depends on Records

Because credit reports provide a structured record of financial behavior, access to certain financial services often depends on the availability of that information.

Without enough credit history, lenders may have limited data to evaluate applications. Understanding how credit scores affect financial life helps explain how these records connect to approvals, deposits, and financing decisions.

Credit history provides the record lenders use to understand financial behavior and evaluate credit access.

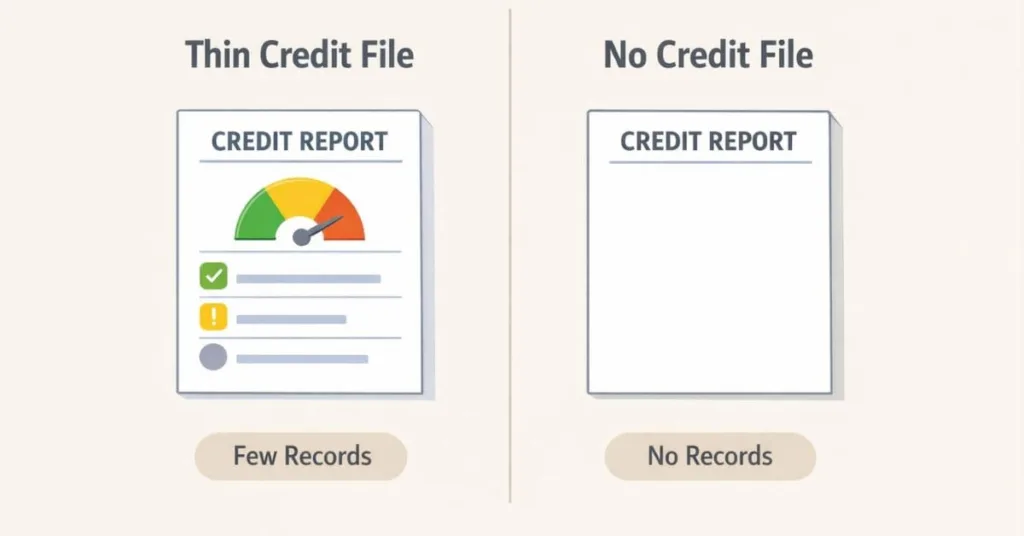

What Is a Thin Credit File?

A thin credit file refers to a credit report that contains only a small amount of credit history. In other words, the credit reporting system has limited information available about a person’s borrowing activity.

This does not necessarily mean someone has bad credit. It simply means there is not enough credit data recorded yet for lenders to fully evaluate financial behavior.

📘 Definition

A thin credit file typically means that a credit report includes only a few credit accounts or a short credit history.

For example, a credit report may show:

- One Credit card account

- A recently opened loan

- Limited payment history

Because credit scoring models rely on historical data, a small amount of recorded activity can make it harder to build a complete credit profile.

🔎 Common Causes

Several situations can lead to a thin credit file.

These may include:

- Recently starting to use credit

- Having only one active credit account

- Rarely using credit products

- Closing older accounts that previously built history

A thin file often occurs during the early stages of credit building.

📄 Examples

A person might have a thin credit file if they:

- Recently opened their first credit card

- Only use one credit account

- Have a short credit history timeline

In these situations, lenders may have limited information available when reviewing applications. Learning how factors like credit utilization work can help beginners understand how credit activity gradually builds a stronger credit profile.

A thin credit file means there is some credit history recorded, but not enough data yet to create a complete credit profile.

What Does No Credit File Mean?

A no credit file situation occurs when the credit reporting system has no recorded credit history for an individual. This means the credit bureaus do not have enough information to generate a credit report.

In simple terms, the system does not yet recognize any credit activity linked to that person.

📄 No Credit History Recorded

When someone has no credit file, it usually means they have never used credit products that are reported to credit bureaus.

Examples may include:

- Never having a credit card

- Never taking a loan

- Not having financing accounts reported to credit bureaus

Without recorded activity, the credit reporting system has no data to build a credit profile.

🔍 Why It Happens

Several situations can lead to a no credit file.

Common reasons include:

- Individuals who have never used credit

- Young adults who have not yet opened credit accounts

- People who prefer using only cash or debit

In these cases, the absence of credit activity means there is no information available for credit reporting systems to track.

🏦 How Lenders Interpret It

When lenders review applications and see no credit file, they may have difficulty evaluating financial reliability.

Without historical data, lenders cannot easily observe patterns such as:

- Repayment behavior

- Account management

- Credit usage history

Because of this limited information, lenders sometimes require additional verification or may rely on alternative evaluation methods.

A no credit file means no credit history exists yet, so lenders have no recorded credit data to evaluate.

Thin File vs No File

Understanding the difference between thin file vs no file helps beginners better interpret how the credit reporting system works. Both situations involve limited credit information, but they are not the same.

The key distinction lies in how much credit history exists and how lenders interpret the available data.

📜 Credit History Length

A thin credit file means that some credit activity has been recorded, but the history is still short or limited.

For example, a person may have:

- Recently opened a credit card

- Only one active credit account

- A short timeline of credit activity

A no credit file, on the other hand, means there is no recorded credit history at all in the credit reporting system.

📊 Available Credit Data

With a thin credit file, credit bureaus have some information available. This may include limited account details and a small amount of payment history.

With no credit file, there is no available credit data for the credit bureaus to report. As a result, a credit report may not exist yet.

🏦 Lender Evaluation Difference

When lenders review a thin credit file, they can still observe some credit activity, even if the data is limited.

However, when there is no credit file, lenders may not have enough information to evaluate credit behavior at all. In these situations, they may rely on alternative information or additional verification.

📊 Thin File vs No File Comparison

| Feature | Thin Credit File | No Credit File |

|---|---|---|

| Credit History | Limited credit history exists | No credit history recorded |

| Credit Accounts | Few accounts present | No credit accounts reported |

| Available Data | Small amount of credit data | No data available |

| Lender Evaluation | Limited information to review | No credit history to evaluate |

A thin credit file contains some credit history, while a no credit file means no credit history exists yet.

Who Usually Has Thin or No Credit Files?

Thin credit files and no credit files are more common than many beginners expect. These situations often occur when someone has limited interaction with credit products or is just beginning to establish a financial history.

Certain groups are more likely to experience these situations due to how credit history develops over time.

🎓 Young Adults

Many young adults have thin or no credit files because they are only beginning to use credit products.

For example, someone who has:

- Recently opened their first credit card

- Never taken a loan

- Only recently started building credit

may have very limited credit history recorded.

🌎 New Immigrants

People who move to the United States often start with no credit file in the US credit reporting system.

Even if they had financial history in another country, that information usually does not transfer to US credit bureaus. As a result, they may begin building credit from the start.

💵 People Avoiding Credit

Some individuals intentionally avoid using credit products and rely only on cash, debit cards, or direct payments.

While this approach can help avoid debt, it may also result in a limited or nonexistent credit history in the reporting system.

📉 Limited Credit Usage

Even people who have credit accounts may still have a thin file if their credit activity is very limited.

For example:

- Using only one credit account

- Having short credit history

- Rarely using available credit

Understanding how credit activity appears on credit reports, including the role of hard vs soft inquiry differences, can help beginners see how credit records develop over time.

Why Lenders Care About Credit History

Credit history helps lenders understand how someone has managed credit responsibilities over time. Because lending involves financial risk, lenders often rely on historical data to evaluate how likely a borrower is to repay obligations in the future.

This historical information becomes an important part of the credit evaluation process.

📊 Risk Evaluation

When reviewing an application, lenders often evaluate potential financial risk.

Credit history can provide signals such as:

- Consistency in payments

- Account management behavior

- Patterns of credit usage

These signals help lenders estimate how reliably someone might manage future credit.

🔄 Borrowing Patterns

Credit reports also reveal patterns of borrowing activity across time.

For example, lenders may observe:

- How frequently credit is used

- How long accounts remain active

- How accounts are managed over time

These patterns provide context beyond a single financial decision.

⚙ Credit Scoring Models

Credit scoring models use information from credit reports to calculate credit scores.

These models typically consider several factors together, including payment behavior, credit usage, and account history. Learning why payment history matters helps beginners understand one of the most important elements used in credit evaluation.

Lenders use credit history to evaluate financial reliability and estimate future borrowing behavior.

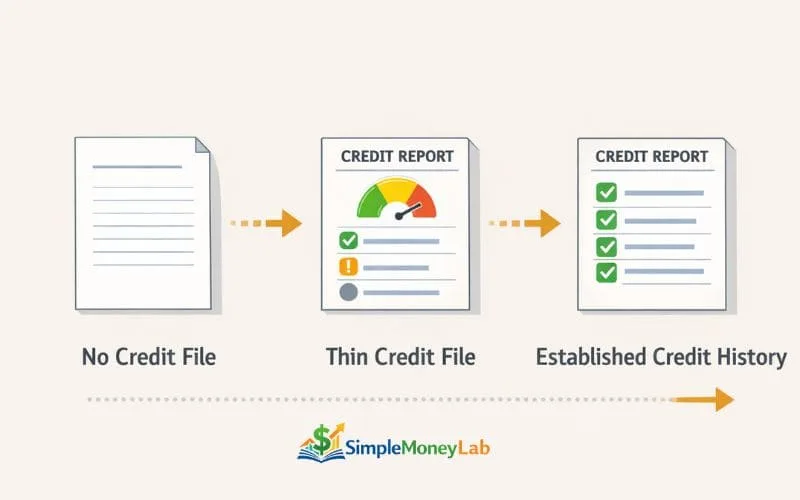

How Beginners Should Think About Thin or No Credit Files

For many beginners, discovering that they have a thin credit file or no credit file can feel discouraging. In reality, this situation is very common when someone is just beginning to interact with the credit system.

Credit history does not appear instantly. It develops gradually as credit activity is recorded over time.

⏳ Credit History Develops Gradually

A credit profile grows slowly as financial activity is reported to credit bureaus.

Each recorded event — such as opening an account or making payments — adds information to a credit report. Over time, these records help create a clearer credit history.

📄 Activity Builds Records

Credit reports expand as more credit activity is documented.

Examples of activity that builds credit records may include:

- Opening Credit Accounts

- Using Credit Responsibly

- Maintaining Active Credit History

As more information appears on a credit report, lenders gain a clearer view of financial behavior.

🧭 Patience > Quick Results

Credit systems are designed to evaluate long-term behavior rather than short-term activity.

Because of this, building a stronger credit history often takes time. Rushing the process is less important than allowing a stable pattern of credit activity to develop naturally.

📈 Long-Term Credit Behavior

Credit history becomes more meaningful as consistent patterns develop across time.

Understanding how long it takes to build credit from zero helps beginners see that credit development is usually a gradual process rather than an immediate result.

Thin or No credit files are simply early stages of credit history, and stronger credit records develop gradually over time.

FAQs

What is a thin credit file?

A thin credit file means a credit report contains only a small amount of credit history. This usually happens when someone has very few credit accounts or has only recently started using credit.

Because credit scoring models rely on historical data, a thin file may provide limited information for lenders evaluating financial reliability.

What does no credit file mean?

A no credit file situation occurs when the credit reporting system has no recorded credit history for an individual. In this case, credit bureaus do not have enough information to generate a credit report.

This often happens when someone has never used credit products such as credit cards or loans.

Is thin credit bad?

Thin credit is not necessarily bad. It simply means there is limited credit history available for evaluation.

However, because lenders rely on credit data to assess risk, a thin credit file may provide less information when reviewing applications.

Can you have a credit score with a thin file?

Yes, it is possible to have a credit score with a thin credit file. If at least some credit activity exists and enough information has been reported, credit scoring models may still generate a score.

However, the score may fluctuate more because there is limited historical data.

How do lenders view no credit history?

When lenders see no credit history, they may have difficulty evaluating financial reliability because there is no past credit activity to review.

In some cases, lenders may request additional information or rely on alternative evaluation methods.

How does credit history start?

Credit history usually begins when a person first opens and uses a credit account that is reported to credit bureaus.

Once activity such as account usage or payments is recorded, credit reporting systems begin building a credit profile over time.

Final Thoughts

Starting with little or no credit history is a very common experience, especially for people who are new to the credit system. Many beginners discover terms like thin file or no file only when they first begin learning how credit reports work.

In reality, credit history does not appear instantly. It develops gradually as financial activity is recorded across time. As accounts are opened, used responsibly, and maintained over longer periods, the credit reporting system begins to build a more complete credit profile.

Understanding how credit history grows helps remove unnecessary confusion. Instead of worrying about limited credit data at the beginning, it becomes easier to see credit building as a long-term process.

Every credit history starts somewhere, and clarity about how the system works makes the journey much easier to navigate.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.