Credit can feel confusing when you’re just starting out. Many beginners in the U.S. hear about credit cards, scores, and reports, but few really understand how the system works or why it matters in everyday life.

A big part of this confusion comes from the fact that credit information is tracked behind the scenes, and most people don’t learn how it works until they need to rent an apartment, apply for a credit card, or finance a car.

At the center of this system is something called a credit report. Your credit report is different from your credit score, and understanding the difference is one of the first steps toward navigating credit with confidence.

This guide breaks down what is a credit report, what it includes, and why it matters—especially for beginners in the U.S. The goal isn’t to overwhelm you, but to explain credit information in plain English so it feels more approachable and less intimidating.

What Is a Credit Report?

A credit report is a detailed record of your credit history, including how you borrow and repay money. In the United States, credit reports are used to evaluate your creditworthiness.

A credit report contains information about your credit accounts, payment activity, and other financial data tied to borrowing. This information is collected from banks, credit card companies, lenders, and sometimes other service providers that report payment behavior. The data is then compiled into a single file that shows how you’ve handled credit over time.

In the U.S., credit reporting operates through a standardized system. Lenders regularly send updates to credit bureaus about whether payments were made on time, how much credit is being used, and whether accounts remain open or closed. The goal of a credit report isn’t to judge how much money you make—it’s to show how reliably you manage money that you’ve borrowed.

What Information Does a Credit Report Include?

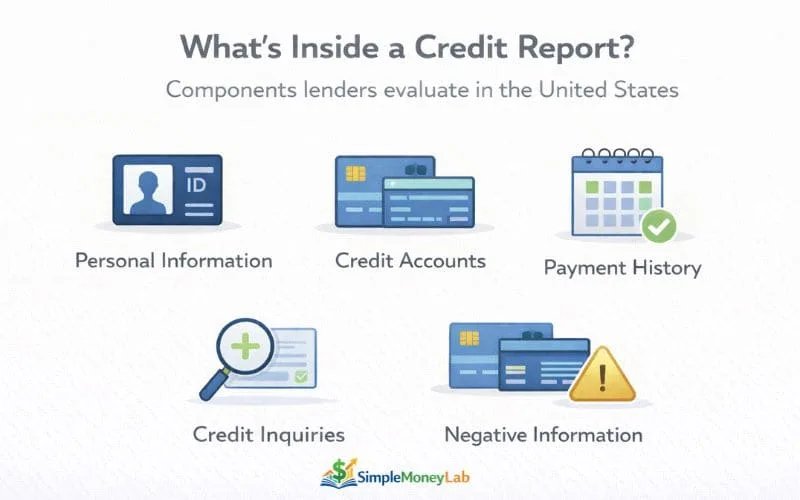

A credit report organizes different pieces of information about your credit history so lenders and other institutions can understand how you’ve managed borrowed money in the past. While formats can vary slightly by credit bureau, most reports include similar categories:

🧾 Personal Information

Includes basic identity details such as your name, date of birth, current and past addresses, and in some cases employment information. This section is used for matching and verification — not for scoring.

💳 Credit Accounts

Shows your open and closed credit accounts, including credit cards, auto loans, student loans, personal loans, and mortgages. It typically lists account type, balance, credit limit, and account status.

📅 Payment History

Shows whether payments were made on time, paid late, or missed. Payment history is considered one of the most important parts of credit reporting because it reflects reliability over time.

➖ Credit Inquiries

Includes both “hard inquiries” (when lenders check your report for credit applications) and “soft inquiries” (checks that don’t affect credit score, such as pre-qualified offers or personal access).

⚠ Negative Information

May include collection accounts, charge-offs, or bankruptcy records if applicable. These items are informational and can influence how lenders evaluate risk.

Who Creates Credit Reports?

In the United States, credit reports are created and maintained by private companies known as credit bureaus or credit reporting agencies. These companies collect credit-related information from lenders and other data furnishers and organize it into a standardized credit file.

The three major nationwide credit bureaus are:

- Equifax

- Experian

- TransUnion

Each bureau independently collects and updates information, which means your credit report may look slightly different depending on the bureau providing it. Not all lenders and creditors report to every bureau, and reporting schedules can vary, which is why consumers may see minor differences across reports from the three companies.

Credit bureaus do not make decisions about whether someone is approved or denied for credit. They supply information that lenders and other institutions may use as part of their own evaluation process.

Why Credit Reports Matter in the US

For many beginners in the United States, credit reports don’t feel important until real-life situations make them suddenly relevant. Because credit reports reflect how reliably a person has handled borrowed money, they’re often used as part of everyday financial decisions — even beyond credit cards and loans.

Here are common situations where credit reports can matter in the U.S.:

🏠 Renting an Apartment

Landlords or property managers may check a credit report to understand a tenant’s payment reliability before approving a lease.

📱 Cell Phone Plans

Major carriers often review credit reports when setting up postpaid plans or financing new devices.

🚗 Auto Loans

Dealerships and lenders may use credit reports to evaluate loan applications for financed or leased vehicles.

💳 Credit Cards

Credit card issuers commonly review credit reports to determine eligibility and assess financial behavior.

📉 Insurance Considerations

Some insurers may use credit-related information as part of their underwriting process in certain states.

⚡ Utilities & Deposits

Utility providers — such as electricity, water, or internet — may check credit reports to decide whether a deposit is required.

These examples show how credit reports can influence everyday access to housing, transportation, communication, and services. Even if someone isn’t borrowing money today, understanding credit reporting early can make future transitions — like moving to a new city or securing a first apartment — much smoother.

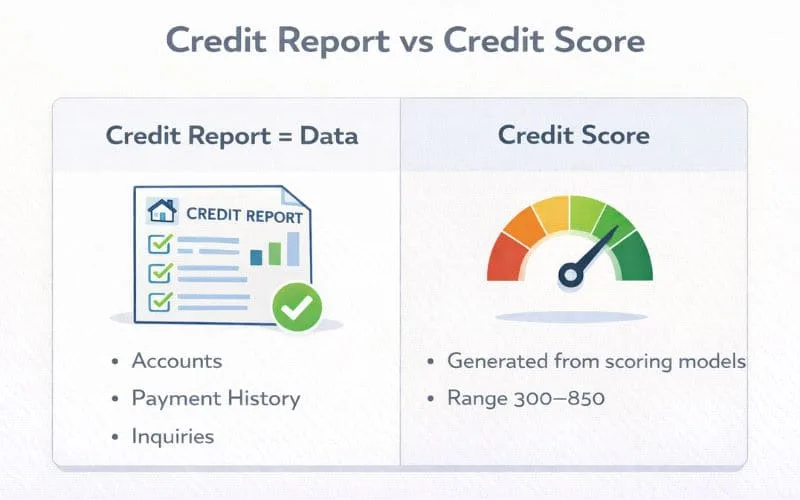

Credit Report vs Credit Score (Key Difference)

Credit reports and credit scores are often mentioned together, but they are not the same thing. The difference is actually simple:

- A credit report is the data

- A credit score is the number created from that data

A credit report contains information about your credit accounts, payment history, and other credit-related details collected over time. Scoring models use that information to generate a three-digit credit score that reflects creditworthiness.

So while a credit report shows the full story, the credit score summarizes that story into a number that lenders can quickly evaluate.

For beginners, understanding this difference makes credit feel less confusing. If you’ve ever wondered how scores are calculated, a credit score is essentially the output of a scoring model applied to the information in your credit report.

How Credit Reports Affect Your Credit Score

Your credit score is directly influenced by the information stored in your credit report. The process is essentially a chain:

Credit Report (data) → Scoring Model (analysis) → Credit Score (number)

Credit reports supply the raw information — such as payment history, account status, and credit usage — while scoring models evaluate that information and convert it into a three-digit score. This makes the credit report the foundation of the scoring process.

In the United States, two major scoring models are commonly used:

✔ FICO — widely used by lenders for loan and credit decisions

✔ VantageScore — another scoring model used across various financial contexts

Each scoring model analyzes the same types of information, but they may weigh certain details differently or update at different times. The important takeaway for beginners is that credit scores don’t exist on their own — they are the result of what’s reported in your credit file. When your report updates, your score may update as well, depending on the model and timing.

For beginners with no credit history, the first credit score appears only after enough data is reported, which raises the common question of how long it takes to build credit from zero.

How Often Do Credit Reports Update?

Credit reports don’t update in real time. In the United States, most lenders and credit card companies send account information to the credit bureaus on a monthly cycle, often tied to billing periods or statement closing dates. As a result, new payments, balances, or account changes typically appear on your report sometime after the lender’s reporting cycle completes.

It’s also important to recognize that credit report updates are not the same thing as credit score updates. While scoring models use the information in your report, they may update on their own timelines once new data is received. That means you may see changes in a report before you see changes reflected in a score, or vice versa, depending on the lender, bureau, and scoring model involved.

Because different lenders report at different times — and not all lenders report to all three major bureaus — updates across Equifax, Experian, and TransUnion may not appear simultaneously. For beginners, the key idea is that credit reporting follows periodic cycles rather than instant updates.

How to Access Your Credit Report (US)

In the United States, consumers can access their own credit reports for review. This process doesn’t affect credit scores and is considered a normal part of understanding how credit information is being reported.

Under federal law, consumers are entitled to request a free credit report from each of the three major credit bureaus — Equifax, Experian, and TransUnion — once per year. AnnualCreditReport.com is the official source that provides access to these reports in one place, without requiring subscriptions or credit card sign-ups.

Accessing your own credit report can help you see what information is being reported, check for accuracy, and understand how lenders view your credit history. For more details on credit reporting rights and consumer protections, the Consumer Financial Protection Bureau (CFPB) offers educational resources on how credit reporting works and what consumers can expect.

Common Misunderstandings About Credit Reports

Credit reports are often misunderstood, especially among beginners who are encountering credit for the first time. Here are some common myths and how the reality actually works:

❌ “My income appears on my credit report.”

Credit reports do not list how much money you earn. They focus on how you’ve managed borrowed money, not your salary or wages.

❌ “Checking my own credit report will lower my score.”

Reviewing your own credit report is considered a soft inquiry and does not affect credit scores. Consumers are allowed to view their own information without penalty.

❌ “Only loans and credit cards show up on a credit report.”

While credit accounts are central, other credit-related items such as inquiries or certain public records can appear as well, depending on reporting practices.

❌ “Only banks look at credit reports.”

Credit reports may be reviewed by landlords, phone carriers, auto lenders, insurers, and utility companies in certain situations as part of access or verification processes.

❌ “A credit report is the same thing as a credit score.”

A credit report contains data; a credit score is a number created from that data. They serve related but different purposes.

❌ “If I have no credit report, it means I have bad credit.”

Having no credit history is not the same as having negative credit. It simply means there isn’t enough information for scoring models to evaluate.

Frequently Asked Questions

What is shown on a credit report?

A credit report includes information about your credit accounts, payment history, account status, credit inquiries, and certain negative items such as collections or bankruptcy records if applicable. It does not include how much money you earn or your personal opinions, savings, or investments.

Does checking my report lower my score?

No. Checking your own credit report is considered a soft inquiry and does not affect your credit score. Consumers are allowed to review their own credit information without triggering a scoring impact.

Do utility bills show up on credit reports?

Most utility bills do not appear on credit reports unless they are reported through specific programs or sent to collections. However, utilities may request access to a credit report when setting up service to determine whether a deposit is required.

Do credit reports include income?

Credit reports do not list your income. They focus on how you’ve managed borrowed money rather than how much you earn. Income may be requested separately during a credit application, but it is not stored in your credit report itself.

Is a credit report the same as a credit score?

No. A credit report contains detailed data about your credit history, while a credit score is a three-digit number generated from that data using a scoring model. The report provides information; the score summarizes it.

Final Thoughts on Credit Reports

Credit reports play a more important role in everyday U.S. life than most beginners realize. They influence access to housing, credit cards, auto loans, mobile plans, and other services that support daily routines. Understanding what’s inside a credit report — and how that information is used — can make the credit system feel less intimidating and more predictable.

You don’t need to memorize every detail or track your credit constantly. What matters most at the beginner stage is building awareness: knowing that credit information exists, knowing where it comes from, and knowing how it affects real-world situations. Over time, that awareness makes it easier to navigate financial decisions with confidence.

Credit isn’t about perfection. It’s about understanding how the system works and learning step by step. For many beginners, simply becoming familiar with credit reports is the first step in building a healthier financial foundation in the U.S.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.