Credit Scores influence more parts of financial life in the United States than most beginners realize. Because credit feels invisible until it’s needed, many people assume it only matters for loans or big financial milestones. In reality, credit can shape everyday access long before someone applies for a mortgage or car financing.

For beginners, this confusion is normal. The US credit system isn’t taught in school, and credit behavior is mostly learned through experience. By the time people encounter credit requirements for renting an apartment, activating utilities, or setting up a phone plan, it often feels surprising.

Credit scores act as a screening tool for risk and reliability, which is why they show up across so many decisions. Understanding how credit scores affect your financial life helps remove anxiety around the system and replaces guesswork with clarity.

Why Credit Scores Matter in the United States

Credit scores play a larger role in the United States than in many other countries because so many everyday systems rely on credit as a risk indicator. In the US, credit isn’t just about borrowing — it’s about access. Screening systems use credit to determine how reliable a consumer may be when entering financial agreements, even for basic services.

This shows up in decisions related to approvals. Landlords, insurers, and service providers often need a way to evaluate applicants quickly, and credit data provides a standardized score that simplifies the process. 📝

Credit also affects pricing. Lower credit can mean higher deposits for utilities, higher insurance premiums, or stricter contract terms. It becomes a form of cost differentiation, where the score influences how much friction a person experiences when trying to secure essential services.

Finally, credit scores serve as a trust signal. Institutions rely on them to assess whether someone is likely to pay on time, fulfill contractual terms, or maintain the account without becoming delinquent. In a system built around contracts, subscriptions, and recurring billing, trust matters.

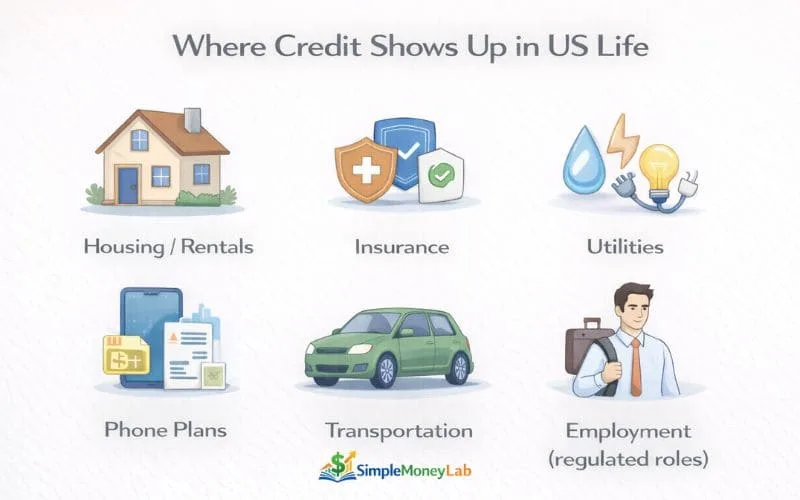

Where Credit Scores Show Up in Everyday Life

Credit scores influence more day-to-day situations than beginners expect. The effects rarely feel dramatic, but they shape how easily people access housing, transportation, essential services, and even communication tools.

Housing & Rentals 🏠

Landlords and property managers often use credit to assess whether tenants will pay rent on time and maintain the lease agreement. Credit affects approvals, security deposits, and, in some cases, additional screening steps. For beginners moving into their first apartment, this is usually the moment when credit becomes visible for the first time.

Insurance Pricing (Auto + Renters) 🚗

Insurance companies in many states use credit-based insurance scores to help estimate predicted risk. While state regulations vary, lower credit scores can sometimes translate into higher auto or renters insurance premiums. Credit doesn’t change eligibility here — it adjusts price and terms.

Utilities & Service Accounts 🔌

When activating electricity, gas, water, or internet services, providers may require deposits from customers with limited or low credit history. Deposits serve as security in case bills go unpaid. Once on-time payments are established, deposits are sometimes returned or credited back.

Cell Phone Plans & Devices 📱

Mobile carriers frequently check credit to approve device financing, installment plans, and postpaid contracts. When credit is thin or lower, beginners may face higher deposits, prepaid plan options, or fewer device financing choices. This experience surprises many because phone plans are seen as basic necessities rather than credit-based products.

Car Financing & Leasing 🚙

Accessing car loans or leases often involves more than just approval — credit affects interest rates, down payment expectations, and financing flexibility. The difference isn’t merely “yes or no,” but how smooth or costly the process becomes. For people in car-dependent cities, transportation decisions make credit highly relevant.

Job & Employment Screening (Contextual) 💼

Some regulated or financial roles may review portions of a candidate’s credit profile as part of compliance requirements. This doesn’t apply to every job and does not create hiring decisions in isolation. It’s more about trust and responsibility in positions where employees manage sensitive financial tasks.

This is often where beginners realize that credit isn’t just about borrowing — it’s a system that affects access and opportunity. Understanding How Credit Scores Work helps make these interactions less surprising and more predictable over time.

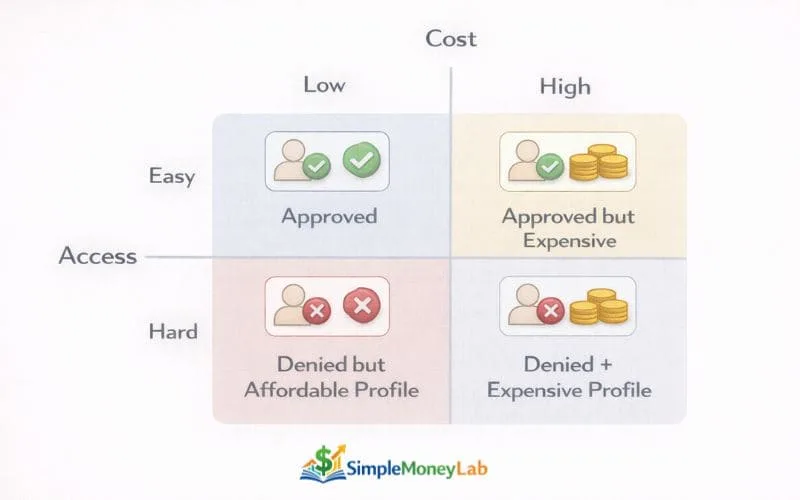

Credit Scores Influence Cost, Not Just Access

One part of the US credit system that surprises beginners is that credit scores don’t only determine whether someone gets approved — they also influence how much that access costs. Two people may receive the same approval, but the financial terms can differ based on credit history.

This price dimension shows up in deposits, monthly premiums, and financing terms. Over time, these small cost differences create noticeable gaps in how affordable everyday financial life feels.

Cost Through Deposits 💳

Deposits are one of the simplest ways credit affects price. Utility providers, property managers, and phone carriers often charge higher upfront deposits to customers with lower or limited credit histories. These deposits are not fees — they function as security during the contract period.

When credit history is stronger, these upfront costs are often reduced or waived, making access smoother with less cash pressure at move-in or activation moments.

Cost Through Insurance Premiums 🚗

Insurance companies in many US states use credit-based insurance scoring to estimate future claim risk. This doesn’t determine eligibility for insurance; it helps price coverage. Consumers with thinner or lower credit profiles may face higher monthly premiums, even when driving history or housing condition is the same.

This pricing logic is rooted in predictive modeling, where credit behavior signals the likelihood of consistent payments and responsible account management.

Cost Through Interest Rates 📉

When financing is involved — such as car loans, personal loans, or leases — credit influences the interest rate, which is the cost of borrowing. Better credit tends to produce smoother approval terms and lower financing costs, while limited credit can lead to higher interest rates or larger down payments to offset perceived risk.

The key point here is not that people with lower credit are denied, but that borrowing becomes more expensive. This is also why How Long it takes to build Credit from Zero matters — stronger credit history gives beginners more flexibility over time.

Why Credit Scores Influence So Many Areas

Credit scores feel unusually powerful in the United States because so many financial and service interactions involve contracts, recurring billing, or delayed payment obligations. Institutions want to know if a consumer will meet those obligations consistently, and credit provides a standardized way to evaluate that risk at scale.

This turns credit into more than a lending tool — it becomes an infrastructure component that supports approvals, pricing, and access across different industries.

Credit as a Risk Signal ⚠️

Companies need ways to judge whether customers will pay on time or maintain accounts responsibly. Credit scores act as a risk signal that estimates probability of repayment. When risk appears higher, institutions may add friction through deposits, higher pricing, or stricter contract terms. When risk appears lower, the path becomes smoother.

Credit behavior patterns influence how lenders evaluate financial risk and access decisions. Learning what is credit utilization helps explain how credit card usage levels can affect how credit behavior is interpreted in real-world financial decisions.

Risk scoring isn’t about moral judgment — it’s about reducing uncertainty in financial transactions.

Credit as a Trust Proxy 🤝

In many service agreements, trust must be established before money exchanges hands. Housing, insurance, phone plans, and utilities often require companies to extend services first and collect payment later. Credit history makes this trust process more efficient by providing a shared reference point for reliability.

This trust dynamic explains why credit shows up in everyday approvals that have nothing to do with borrowing.

Credit as a Contract Compliance Tool 📄

The US economy relies heavily on contracts — rentals, leases, subscriptions, financing plans, and recurring services. Credit helps signal whether someone is likely to fulfill those commitments without defaulting. Instead of running custom evaluations for every applicant, companies use standardized credit data for faster, lower-cost compliance checks.

Even regulatory research from federal agencies such as the Consumer Financial Protection Bureau (CFPB) highlights how credit functions as a system for managing contractual risk in consumer markets.

Misconceptions Beginners Have About Credit Scores

Beginners often underestimate how widely credit influences financial life because early exposure to credit usually happens through borrowing. This leads to misunderstandings about what credit affects, when it becomes relevant, and why it shows up in places that don’t involve debt at all.

These misconceptions are common, especially during the first few years of financial independence.

“Credit Only Matters for Loans”

Many people assume credit scores only matter when applying for credit cards, auto loans, or mortgages. While credit does affect borrowing, the system also influences access to housing, insurance pricing, deposits for utilities, and phone plan approvals. In the US, these services rely on credit because they involve delayed payment or contract-based billing, not just lending.

“Debt-Free Means Credit-Free”

Another misconception is that avoiding debt removes the need for credit entirely. Being debt-free may feel financially clean, but it doesn’t build credit history. Without history, beginners may encounter higher deposits or additional verification when starting new services. Credit is less about borrowing and more about demonstrating reliability in financial agreements.

“I’ll Worry About Credit Later”

Many beginners push credit off until adulthood milestones like renting, relocating, or financing a car. The challenge is that credit takes time to build. When the need arrives suddenly, beginners may face friction while starting from zero. This is one reason Underestimating Credit Impact becomes a common money mistake during early financial transitions.

📍 Key Idea: Delaying credit doesn’t avoid credit — it delays flexibility.

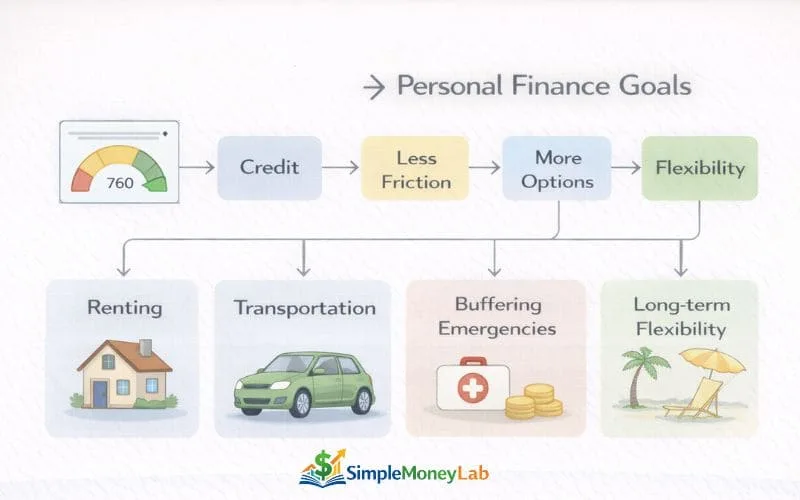

How Credit Scores Connect to Personal Finance Goals

Credit doesn’t exist in a vacuum. It connects directly to the personal finance goals beginners care about the most: access to housing, transportation, stability, and flexibility. These goals are often discussed as budgeting or saving problems, but credit frequently determines how smooth or expensive the path becomes.

When beginners understand this bridge, credit stops feeling like a technical system and starts feeling like part of everyday financial planning.

Renting & Relocating 🏠

Moving is one of the first moments credit becomes unavoidable. Landlords and property managers check credit for lease approvals, security deposits, and sometimes co-signer requirements. Even if rent itself isn’t financed, the leasing agreement still involves future payment obligations — which is why credit shows up.

This connects housing decisions to financial preparation, not just budgeting.

Car Access & Transportation 🚗

Transportation is another area where credit influences options. Buying or leasing a car typically involves financing, but even beyond loans, some dealerships evaluate credit before offering Lease terms, Interest rates, or Down Payment expectations. Without reliable transportation, commuting to work or school becomes harder, making credit indirectly relevant to income stability.

Buffering Surprise Expenses 💸

When unexpected expenses hit — car repairs, medical bills, or travel — people without cash buffers often turn to credit as a temporary bridge. This makes emergency funds and credit-building complementary rather than competing strategies. A future article on Emergency Buffers expands on why small savings cushions reduce stress during financial shocks.

Future Flexibility 🔄

The long-term benefit of credit is optionality. Credit doesn’t just determine whether someone can access a service — it influences how many choices they get, how much friction they face, and how much it costs. When beginners understand their cash flow through Budget basics and build credit gradually, they gain more flexibility during major life decisions.

Personal finance isn’t only about handling money you have — It’s also about reducing the cost of the money you need access to.

How Beginners Can Approach Credit Gradually

Many beginners assume improving credit requires big financial changes, specialized tools, or perfect budgeting. In reality, credit systems tend to reward consistency more than intensity. Small, repeatable behaviors shape credit history over time because the system measures patterns rather than isolated actions.

This gradual approach reduces pressure. When beginners focus on visibility — understanding how payments, balances, and timing interact — credit feels less mysterious and more predictable. Visibility creates familiarity, and familiarity makes credit less stressful.

Perfection isn’t required. Credit systems tolerate delays, fluctuations, and life events; what matters is how the overall pattern looks across months and years. This is why credit is often described as a timeline instead of a scoreboard — Building Credit from Zero takes time because history itself needs time to form.

Credit is less about optimizing and more about staying consistent.

FAQs About How Credit Scores Affect your Financial Life

Does Credit score matter if I never borrow?

Yes. In the United States, credit scores influence more than just borrowing. Even if someone avoids credit cards or loans, credit scores can affect access to rentals, utility accounts, cell phone plans, and insurance pricing. Many of these services involve billing or contracts where companies need to assess reliability. Because of that, credit functions as a trust and risk indicator, not just a borrowing tool.

What everyday things are affected by Credit score?

Credit scores can affect housing approvals, insurance premiums, security deposits for utilities, cell phone plan eligibility, and in some cases financing offers for vehicles or personal purchases. Credit also plays a role in relocations, moving between states, and starting new service accounts. The effects are rarely visible until someone needs to activate these services for the first time.

Can beginners build Credit without debt?

Yes. Credit history can be built without carrying debt or paying interest. Credit systems reward consistent account activity, on-time payments, and established history rather than outstanding balances. Some people use products designed for thin credit profiles to establish history, while others build credit through recurring payments on existing accounts. The key factor is history, not the presence of debt.

How long does it take to improve Credit?

It depends on the person’s situation and what part of the credit profile is being measured. Credit systems evaluate patterns over time, so changes are not instant. Establishing credit from zero typically takes months to begin showing scores and longer to build depth. Improvements related to payment consistency and balances may register faster, while history-based factors require more time because age cannot be accelerated.

Why does the US use Credit scores?

The United States uses credit scores to create a standardized way for companies to assess repayment risk and contract compliance. Because many services provide access first and collect payment later, the system requires a reliable method to evaluate applicants. Credit scores reduce friction by offering a shared metric that lenders, insurers, landlords, and service providers can interpret without custom evaluation for each case.

Do employers check Credit?

Some employers may review portions of a person’s credit file for roles involving financial responsibility, sensitive information, or regulatory compliance. This does not apply to most jobs and is not used to determine income potential or job performance. It is more about assessing accountability in positions where handling money or sensitive data is part of the role. Credit checks in hiring are regulated and require consent.

Final Thoughts

Credit can feel complicated to beginners because most people first encounter it at the moment of need, not during a moment of preparation. That timing creates stress and confusion, but the gap itself is normal. The US credit system isn’t something people are taught in school, and adults are often expected to navigate it quietly on their own.

When credit is reframed as part of everyday access — housing, utilities, transportation, and communication — it becomes easier to understand why the system influences so many areas of financial life. Credit isn’t about perfection; it’s about patterns that unfold over time.

Once beginners gain clarity around budgeting, bills, and credit, the next stage of personal finance often includes exploring income flexibility. Many people look into Side hustles for beginners once stability improves, because earning becomes easier to manage when the financial foundation feels less reactive.

Financial progress is less about catching up and more about replacing uncertainty with understanding.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.