Unexpected expenses are one of the biggest reasons people feel financially stressed, especially when money is already allocated to monthly bills. In the United States, costs like medical visits, urgent repairs, or sudden travel can appear without warning. When these events happen, the financial pressure often comes from timing — not just from the cost itself.

Not having emergency savings is more common than many beginners think. Rising living costs and income timing gaps make it difficult for many households to keep extra money set aside for unknown situations.

Understanding what is an emergency fund helps explain how people protect themselves from these financial shocks. An emergency fund is not about building wealth — it is about creating a financial buffer that helps stabilize daily life when unexpected expenses happen.

Why Emergency Funds Matter in Real Life

Unexpected expenses rarely happen at convenient times. For many US households, most income is already assigned to rent, groceries, transportation, and other recurring costs. When a sudden expense appears outside that schedule, the disruption often feels bigger than the actual dollar amount.

In real life, financial stress usually comes from timing — not just from how much something costs.

Emergency funds exist because financial life does not move in perfect monthly cycles. Income follows predictable patterns, but emergencies do not. When unexpected expenses appear between pay cycles or during already tight months, financial pressure increases quickly.

Several real-world factors explain why emergencies feel financially disruptive:

- Unexpected Cost timing — Emergency expenses appear outside normal billing cycles

- Financial Shock events — Sudden costs require immediate decisions

- Income vs Expense timing mismatch — Paychecks follow schedules, emergencies don’t

- US Cost spikes — Healthcare, Urgent repairs, and Emergency services can be expensive and immediate

For many beginners, the difference between financial stability and financial stress is not income level alone — it is whether a buffer exists when timing breaks.

In practical terms, emergency funds don’t eliminate unexpected expenses. They help prevent those expenses from disrupting normal financial routines and decision-making.

Emergency funds reduce the financial impact of bad timing — not just unexpected costs.

What Is an Emergency Fund?

In real life, unexpected expenses don’t wait until a financially convenient time. This is why emergency funds exist — not as extra savings, but as financial protection. For many beginners, this is the first time they learn that not all savings serve the same purpose.

An emergency fund is money set aside specifically to cover unexpected financial events. It acts as a financial buffer when unplanned expenses or sudden income interruptions happen, helping protect normal monthly financial routines.

Emergency funds are designed for stability, not growth. Their goal is to reduce disruption when financial surprises appear.

Real-Life Meaning

In everyday life, an emergency fund helps people handle situations such as:

- Sudden Medical costs

- Urgent Home or Car repairs

- Temporary Income disruption

- Emergency Travel or Family needs

For many US households, these costs are not rare events — they are timing events. Emergency funds help smooth the financial impact when life becomes unpredictable.

Understanding income flow helps explain how emergency funds are built over time. Learning what is disposable income helps beginners see how usable income can gradually support financial protection buffers.

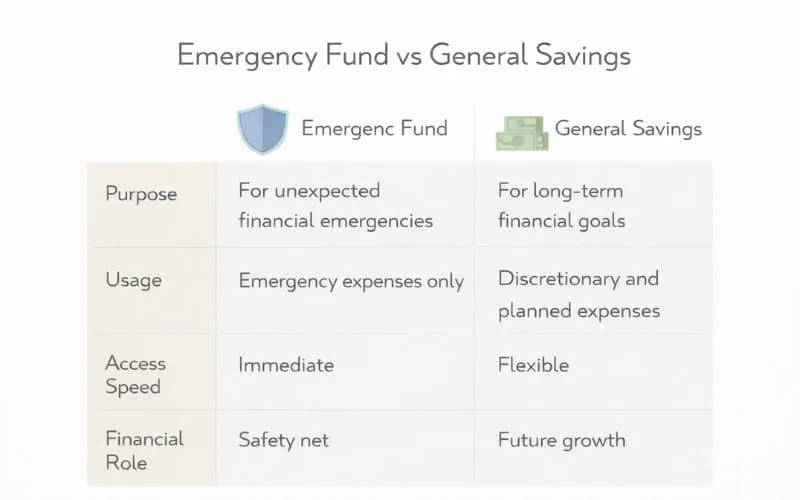

Emergency Fund ≠ General Savings

Emergency funds are often confused with general savings, but their purpose is different.

General savings are usually used for planned goals like Vacations, Purchases, or Future lifestyle expenses. Emergency funds exist only for urgent, unexpected financial disruptions.

Mixing these two types of savings can reduce financial protection during real emergencies, because protection money may already be allocated for planned spending.

In simple terms:

- General Savings = Planned spending

- Emergency Fund = Financial protection

An Emergency fund is protection money — not goal money.

How Emergency Funds Protect Everyday Financial Stability

In real life, financial stability is less about avoiding unexpected expenses and more about being able to absorb them when they happen. For many US households, monthly finances run on tight schedules, and even one unexpected cost can disrupt multiple financial commitments at once.

Emergency funds help stabilize financial routines by creating a buffer between unexpected events and everyday financial obligations.

🛡 Shock Absorption

Emergency funds act as a financial shock absorber when sudden costs appear.

Common examples include:

- 🏥 Unexpected Medical bills

- 🔧 Urgent Car or Home repairs

- ✈️ Emergency Travel needs

- 📉 Short-term Income gaps

Instead of forcing immediate financial changes, a buffer helps absorb the impact and maintain normal spending patterns.

🔄 Decision Flexibility

When a financial buffer exists, decisions usually feel less rushed.

Emergency funds can help create:

- ⏳ More time to evaluate options

- 🧠 Less pressure to make fast financial decisions

- 📊 Better ability to compare solutions

Without a buffer, financial decisions often become reaction-based rather than choice-based.

🧠 Stress Reduction

Financial buffers can reduce emotional stress during unexpected situations.

This often means:

- Fewer Panic-driven financial decisions

- More Confidence handling disruptions

- Clearer thinking during emergencies

Financial stability is not only about money availability — it also affects decision clarity.

📉 Borrowing Pressure Reduction

Emergency funds can reduce immediate pressure to rely on borrowing during urgent situations.

This can help lower:

- Forced Credit usage

- Urgent High-cost borrowing decisions

- Long-term Financial recovery stress

Emergency funds protect financial stability by reducing urgency, not just covering costs.

Why Many Beginners Struggle to Build Emergency Funds

For many beginners, not having an emergency fund is not a discipline problem — it is a financial bandwidth problem. When most income is already assigned to essential expenses, building financial protection can feel unrealistic or delayed.

In real life, emergency savings are often postponed because immediate financial needs feel more urgent than future risks.

💵 Income Pressure

When income is tightly allocated, financial buffers become harder to build.

Common income pressure areas include:

- 🏠 Housing costs

- 🚗 Transportation costs

- 🛒 Groceries and Daily essentials

- 🧾 Insurance and Minimum debt payments

When most income is committed, emergency savings often feel like a “later” goal instead of a current financial layer.

🏙️ Cost of Living Pressure

Rising costs can reduce financial breathing room.

This can show up through:

- 📈 Rent increases

- 🧾 Insurance Premium changes

- 🛒 Grocery Price volatility

- ⚡ Utility Cost fluctuations

When essential costs rise faster than income, building financial buffers becomes more difficult.

🧠 Money Overwhelm

Many beginners manage multiple financial learning curves at once.

Examples include:

- Budgeting basics

- Credit understanding

- Debt management

- Income planning

- Savings structure

When money feels complicated, emergency savings often move lower on the priority list.

⏳ Delayed Priority Thinking

Future financial risks often feel less urgent than current expenses.

This usually happens because:

- Future emergencies feel abstract

- Current bills feel immediate

- Short-term needs feel more visible than long-term protection

Spending visibility often develops before buffer awareness. Learning How to track Spending without Overwhelm helps beginners see where small financial cushions may gradually become possible over time.

Most beginners struggle to build emergency funds because of financial pressure and complexity — not lack of discipline.

US-Specific Reasons Emergency Funds Matter More

In the United States, emergency funds often play a bigger role because many essential costs can change quickly and without much warning. Unlike systems where Healthcare, Repairs, or Income stability are more predictable, US households often need to manage higher cost variability across multiple life areas.

For many beginners, emergency funds are not just savings tools — they are financial stability tools designed to handle system-level uncertainty.

🏥 Healthcare Risk

Healthcare costs in the US can vary widely depending on coverage and timing.

Unexpected healthcare costs can include:

- Emergency room visits

- Out-of-network charges

- Deductible resets

- Prescription cost changes

Even insured households can face sudden out-of-pocket costs.

🛡 Insurance Gaps

Insurance does not always cover every cost immediately.

Common gap areas can include:

- Coverage waiting periods

- Deductible thresholds

- Partial Claim approvals

- Excluded Service categories

These gaps can create short-term financial pressure even when insurance exists.

💼 Job Instability and Income Variability

Income stability can vary depending on job structure.

Some income risks include:

- Layoffs or Restructuring

- Contract or Gig income gaps

- Reduced work hours

- Delayed bonus or Commission income

Emergency funds help stabilize living costs when income timing changes.

🔧 Repair Cost Spikes

Essential repairs often cannot be delayed and may cost more when urgent.

Examples include:

- Car breakdown repairs

- Heating or Cooling system failures

- Plumbing emergencies

- Appliance replacement

Urgent repairs often cost more due to timing pressure.

💳 Credit Reliance System

The US financial system often expects access to credit during emergencies.

This can create pressure to rely on borrowing if no buffer exists.

Emergency funds can help reduce dependence on emergency borrowing during urgent situations.

Emergency funds help manage system-level financial uncertainty in the US — not just unexpected expenses.

Emergency Fund vs General Savings

Many beginners assume all savings serve the same purpose, but in real life, savings usually exist in different layers. Some savings support planned goals, while others exist purely to protect financial stability during unexpected events.

Understanding this difference helps prevent using protection money for planned expenses and helps maintain financial stability when emergencies happen.

🎯 Purpose Difference

Emergency funds and general savings exist for different financial reasons.

Emergency fund purpose:

- 🛡 Financial Protection

- ⏳ Unexpected event support

- 📉 Income disruption coverage

General savings purpose:

- ✈️ Planned travel

- 🛍 Planned purchases

- 🏡 Future Planned expenses

Emergency funds focus on stability.

General savings focus on planning.

💳 Usage Difference

How these savings are used is also different.

Emergency funds are typically used only during urgent, unexpected situations.

General savings are usually used for:

- Scheduled expenses

- Known upcoming purchases

- Lifestyle planning

Mixing these purposes can reduce financial protection during real emergencies.

🏦 Accessibility Difference

Emergency funds are usually kept in places that are:

- ⚡ Quick to access

- 📊 Stable in value

- 💰 Separate from daily spending money

General savings may be stored in accounts meant for medium or long-term goals where access timing is less urgent.

In real life, accessibility often determines whether savings can actually function as an emergency buffer.

Emergency funds protect stability, while general savings support planned financial goals.

How Beginners Can Think About Emergency Funds

For many beginners, emergency funds feel intimidating because they are often presented as large savings goals instead of financial protection tools. In real life, financial stability usually builds through consistency and awareness, not through perfect saving timelines.

When emergency funds are framed as protection instead of achievement, they often feel more realistic and less overwhelming.

Many US beginners find emergency savings easier to understand when they shift from goal pressure to protection mindset.

🛡 Protection > Perfection

Emergency funds work as protection layers, not performance metrics.

- Protection focuses on financial safety

- Perfection focuses on ideal outcomes

- Safety thinking reduces pressure

Financial protection usually builds gradually, not perfectly.

🧱 Stability > Speed

Financial stability usually matters more than how quickly savings grow.

- Stability supports consistent financial routines

- Speed-focused saving can feel stressful

- Steady progress usually feels more sustainable

Emergency funds support long-term financial calm, not fast financial milestones.

🔁 Consistency > Size

Consistency often matters more than total savings size at the beginning.

- Regular awareness builds financial habits

- Consistency improves financial confidence

- Small repeated progress often feels more manageable

Financial behavior patterns usually shape long-term stability more than single large savings events.

🧠 Buffer Mindset > Target Chasing

Thinking in terms of financial buffers often reduces stress compared to chasing fixed savings targets.

- Buffers focus on protection

- Targets focus on achievement

- Protection thinking supports long-term financial resilience

In real life, financial buffers help create decision space during unexpected events.

Emergency funds work best when seen as protection layers, not performance goals.

FAQs

What is an emergency fund?

An emergency fund is money set aside specifically for unexpected financial situations such as medical bills, urgent repairs, or sudden income interruptions. It is designed to act as a financial buffer that helps protect normal monthly expenses when something unplanned happens.

In personal finance, emergency funds are considered protection savings rather than goal savings. Their main purpose is to help reduce financial disruption during stressful or unpredictable situations.

Why is an emergency fund important?

An emergency fund is important because unexpected expenses can happen at any time, and without a financial buffer, these costs can quickly disrupt normal financial routines. Emergency funds help reduce the need to make rushed financial decisions during stressful moments.

They also help create financial flexibility, giving people more time to evaluate options when unexpected costs appear.

Is an emergency fund the same as savings?

No, an emergency fund is not the same as general savings. Emergency funds are meant only for unexpected and urgent financial situations. General savings are usually meant for planned expenses such as travel, purchases, or future goals.

Keeping these two types of savings separate helps maintain financial protection when emergencies happen.

When should an emergency fund be used?

Emergency funds are typically used during situations that are unexpected, urgent, and necessary. This can include sudden medical costs, urgent repairs, or temporary income interruptions.

They are usually not meant for planned expenses or lifestyle purchases.

Can an emergency fund start small?

Yes, emergency funds often begin small and build gradually over time. Many beginners focus first on creating financial awareness and stability before building larger financial buffers.

Consistency and understanding financial patterns often matter more than starting with large savings amounts.

Where is an emergency fund usually kept?

Emergency funds are usually kept in places that are easy to access quickly and that keep money stable in value. The goal is accessibility and reliability rather than growth or long-term investment.

Emergency funds are typically separated from daily spending money to reduce accidental use.

Final Thoughts

Not having an emergency fund is more common than many beginners realize. Financial protection usually develops over time, especially as income visibility, spending awareness, and financial confidence grow. Learning how financial buffers work is part of building long-term financial stability.

Emergency funds are not about financial perfection. They are part of learning how money systems work in real life, especially in environments where costs, income timing, and unexpected expenses can change quickly. Financial stability is often built through understanding and consistency rather than speed.

Over time, emergency funds become less about saving money and more about creating financial breathing room. When financial buffers exist, unexpected situations often feel more manageable and less disruptive.

As financial protection improves, many beginners naturally start exploring how money behavior connects to other areas of financial life, including credit systems and long-term financial access.

Financial stability is a skill that develops through understanding, awareness, and gradual financial structure building.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.