Many beginners feel unsure about how credit really works in everyday life. It’s common to hear that credit scores matter, but less clear to understand how credit scores affect financial life beyond just loans. This confusion can create unnecessary fear or avoidance, especially for people who are still learning how the US credit system operates.

In reality, credit scores are not just about borrowing money. They influence access, approvals, deposits, and sometimes even pricing across different areas of financial life. Understanding how credit scores affect financial life helps shift the focus from fear to clarity.

In the United States, credit scores act as a reliability signal in many systems. They don’t define a person’s worth — but they often influence how financial institutions evaluate risk and trust.

How Credit Scores Affect Financial Life in the US

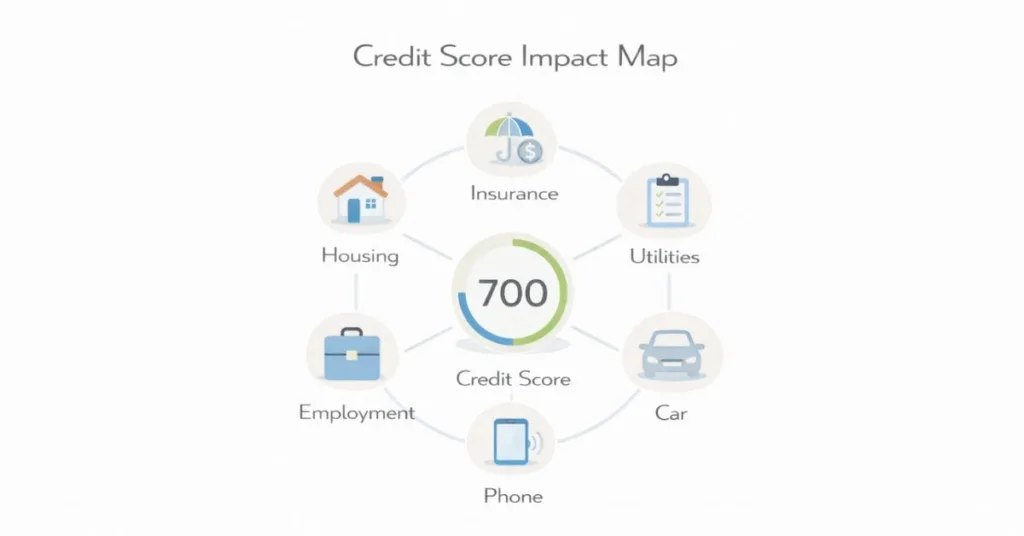

Credit scores influence more than just loan approvals. In the United States, they are often used as a reliability signal across multiple financial systems. This can affect both access to services and the cost of using them.

Understanding these real-life touchpoints helps clarify how credit scores affect financial life in practical ways.

🏠 Housing & Rentals

Landlords and property managers may review credit reports during rental applications.

Credit scores can influence:

- Approval decisions

- Security deposit requirements

- Co-signer requests

- Rental screening outcomes

Credit information helps landlords evaluate payment reliability.

🚗 Insurance Pricing

In many states, insurers use credit-based insurance scores as part of pricing models.

This can affect:

- Auto insurance premiums

- Renters insurance costs

- Policy eligibility factors

Insurance pricing models use risk assessment tools, and credit behavior may be one component.

⚡ Utilities & Service Deposits

Utility providers sometimes review credit history when opening new accounts.

This may impact:

- Deposit requirements

- Payment plan approvals

- Account setup conditions

Lower perceived risk can reduce deposit requirements in some situations.

📱 Cell Phone Plans

Mobile carriers may review credit during:

Device financing approvals

Contract-based plan approvals

Installment agreements

Credit evaluation can influence whether a deposit is required for devices or service plans.

🚘 Car Financing

Auto lenders often use credit scores when determining:

- Approval eligibility

- Interest rate ranges

- Down payment requirements

Since loan pricing depends on risk assessment, understanding how credit scores work helps explain why financing terms can vary between applicants.

💼 Employment Screening

Some employers, especially in financial or regulated roles, may review credit reports as part of background checks.

This is typically:

- Industry-specific

- Regulated by state laws

- Not universal across all jobs

Credit checks in employment are generally used to assess financial responsibility for certain sensitive positions.

In the US system, credit scores can influence both access and cost across housing, insurance, utilities, financing, and select employment situations.

Credit Scores Affect Cost, Not Just Approval

Many beginners think credit scores only determine whether something is approved or denied. In reality, credit scores often influence the cost of financial access — not just access itself.

In the US system, credit scores are frequently used as pricing signals.

💰 Interest Rates

Lenders often use credit scores to assess perceived repayment risk.

This may influence:

- Loan interest rate ranges

- Financing terms

- Repayment structure options

Even when approval is granted, pricing can vary depending on overall credit profile. Understanding factors like credit utilization helps explain how behavior patterns influence how risk is evaluated.

🧾 Deposit Requirements

Credit history can affect upfront deposits for services such as:

- Rental agreements

- Utility accounts

- Financed devices

Lower perceived risk may reduce deposit requirements in certain situations, while higher perceived risk may increase them.

🚗 Insurance Premium Variation

In many states, insurers incorporate credit-based risk indicators into pricing models.

This can influence:

- Premium calculations

- Eligibility tiers

- Payment flexibility options

Insurance pricing decisions often involve multiple factors, with credit behavior sometimes being one component.

🔄 Financing Flexibility

Credit scores can influence how flexible financing options may be.

This may affect:

- Payment plan structures

- Promotional offers

- Refinancing eligibility

- Loan term customization

Higher financial reliability signals may increase flexibility in structuring agreements.

Credit scores often influence how much something costs — not just whether access is granted.

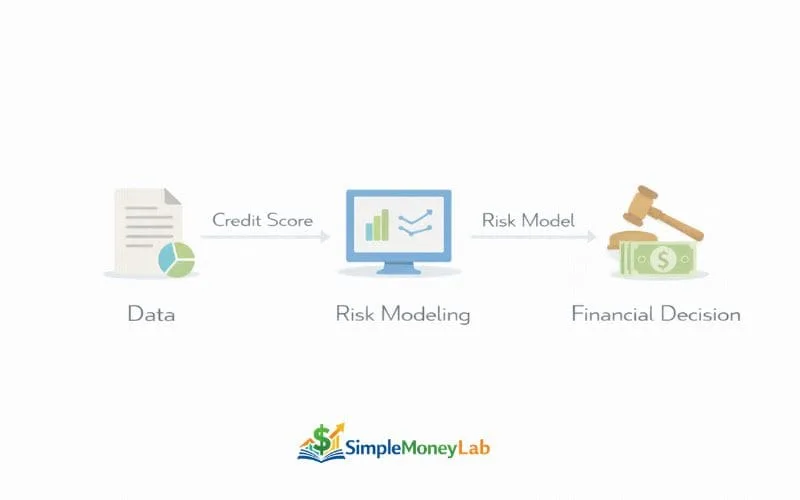

Why the US Uses Credit Scores So Broadly

Credit scores are widely used in the United States because they function as standardized risk signals across large financial systems. Instead of evaluating every applicant manually, institutions rely on structured scoring models to assess patterns of financial behavior.

This system helps create consistency across markets.

📊 Risk Modeling

Credit scores are built using statistical risk modeling.

Financial institutions use scoring systems to:

- Evaluate repayment patterns

- Compare applicants consistently

- Estimate probability of future repayment behavior

Credit scoring systems are built on large-scale consumer credit data and repayment behavior patterns. The Federal Reserve’s research on household financial experiences, including its Consumer Credit and Financial well-being research, explains how credit access and repayment behavior are analyzed across the US financial system to evaluate risk and predict repayment outcomes.

Risk modeling allows institutions to process large volumes of applications efficiently.

📑 Contract Reliability

In many cases, credit scores are used as a proxy for financial reliability.

Institutions may interpret credit behavior as signals of:

- Consistency

- Obligation management

- Contract performance history

While not perfect, credit scores offer a standardized way to evaluate financial reliability in contractual agreements.

📈 Predictive Analytics

Credit scoring systems rely on predictive analytics rather than personal judgment.

This means:

- Scoring is data-driven

- Decisions are model-based

- Outcomes are standardized

Predictive systems attempt to forecast repayment likelihood using historical behavior patterns.

🏛 Market Standardization

Because multiple lenders, insurers, and service providers use credit scores, they have become embedded in the broader US financial infrastructure.

This standardization:

- Reduces manual underwriting costs

- Speeds up approvals

- Creates common evaluation benchmarks

Credit scores are widely used in the US because they provide standardized, data-driven risk evaluation across financial markets.

Common Beginner Misunderstandings

Credit scores often feel mysterious because they are rarely explained clearly in everyday education. Many beginners carry assumptions that sound logical — but don’t fully match how the US financial system actually works.

Clarifying these misunderstandings helps reduce unnecessary stress and improve financial awareness.

💳 “Credit Only Matters for Loans”

Many people believe credit scores only affect borrowing money.

In reality, credit information may also influence:

- Rental applications

- Insurance pricing

- Utility deposits

- Financed devices

Because credit is often used as a reliability signal, its impact can extend beyond traditional loans.

💵 “Cash Users Don’t Need Credit”

Some beginners assume that paying with cash or debit removes the need for credit awareness.

While cash use avoids borrowing, certain systems in the US may still evaluate credit history when assessing:

- Housing applications

- Service contracts

- Installment agreements

Using cash does not automatically remove credit from the broader financial landscape.

⏳ “Credit Only Matters Later in Life”

Another common belief is that credit scores only become important when applying for major loans.

In practice, credit awareness can matter earlier than expected — especially during:

- First apartment searches

- First car financing

- Relocating to new cities

- Opening new utility accounts

Learning from common beginner money mistakes helps connect credit misunderstandings to broader financial learning patterns.

Credit misconceptions often come from incomplete information, not from financial failure.

How Credit Scores Connect to Personal Finance Stability

Credit scores are not just approval numbers — they can influence overall financial stability. In the US system, credit often functions as a flexibility tool. When understood clearly, it becomes part of long-term financial planning rather than a short-term stress point.

Credit and stability are connected through access, cost, and financial resilience.

🛟 Emergency Resilience

In urgent situations, financial flexibility matters.

Credit history can sometimes influence:

- Access to financing options

- Payment plan eligibility

- Short-term borrowing terms

While savings are the foundation of stability, understanding Emergency Fund basics helps show how savings and credit awareness work together in unexpected situations.

📦 Relocation Flexibility

Moving to a new city or apartment often involves:

- Rental screening

- Deposit requirements

- Utility setup

Credit scores may influence how smoothly these transitions happen.

Financial stability often includes the ability to relocate without excessive friction.

🤝 Financial Negotiation Power

Stronger financial reliability signals can sometimes increase flexibility in structured agreements.

This may influence:

- Loan structuring options

- Refinancing eligibility

- Installment agreement terms

Credit history can affect how institutions structure financial offers.

🔓 Long-Term Access

Over time, financial systems evaluate patterns of behavior.

Consistent credit reliability may influence:

- Long-term financing eligibility

- Service account access

- Contract flexibility

Financial stability often includes predictable access to financial systems without unexpected barriers.

Credit scores can influence financial stability by shaping access, flexibility, and cost across different life stages.

How Beginners Can Think About Credit Scores

Credit scores often feel personal, especially when the number changes. In reality, credit systems measure behavior patterns over time. Shifting the mindset from short-term reactions to long-term reliability helps reduce unnecessary stress.

Understanding the system makes credit feel more predictable.

🔁 Reliability > Perfection

Credit systems are designed to evaluate consistency.

- Long-term on-time payments matter

- Stable account behavior builds trust signals

- Small fluctuations are common

Credit growth is usually about steady reliability rather than flawless history.

📊 Pattern > Panic

One payment or one billing cycle rarely defines overall credit health.

- Trends across months matter more

- Consistent reporting builds stronger signals

- Temporary changes are normal

Credit scores reflect patterns, not isolated moments.

🧠 System Awareness > Fear

Many credit worries come from not knowing how reporting cycles work.

Understanding:

- Reporting timelines

- Scoring recalculations

- Multi-bureau differences

helps reduce confusion and emotional reactions.

⏳ Long-Term Stability Mindset

Credit systems operate on timelines, not instant reactions.

Learning how long it takes to build credit from zero helps connect credit scores to long-term financial development rather than short-term movements.

Over time, steady behavior tends to shape stronger financial reliability signals.

Credit scores respond to long-term behavior patterns — not momentary perfection.

FAQs

How do credit scores affect financial life?

Credit scores affect financial life by influencing approvals, pricing, deposits, and access to certain services. In the US, they are often used as risk signals by lenders, landlords, insurers, and service providers.

Rather than defining financial success, credit scores typically function as standardized tools that help institutions evaluate reliability.

Does a credit score affect renting?

In many rental situations, landlords may review credit reports during the screening process. Credit history can influence approval decisions, deposit requirements, or co-signer requests.

Rental policies vary, but credit information is commonly part of the evaluation process.

Does a credit score affect insurance?

In many states, insurers use credit-based insurance scores as part of pricing models. Credit behavior may be one of several factors considered when determining premium levels.

Insurance pricing decisions usually combine multiple risk indicators.

Can you live without credit in the US?

It is possible to operate primarily with cash or debit. However, certain systems in the US — such as rentals, financed purchases, or some service contracts — may still review credit history.

Because of this, understanding credit can improve flexibility within the financial system.

Why do employers check credit?

Some employers, particularly in financial or regulated roles, may review credit reports as part of background screening. This practice is usually limited to specific industries and governed by federal and state laws.

Not all jobs require credit checks.

Does a credit score affect deposits?

Credit history can influence deposit requirements for rentals, utilities, or financed services. In some cases, stronger credit reliability may reduce upfront deposit amounts.

Deposit policies vary depending on the provider and local regulations.

Final Thoughts

Understanding how credit works often takes time, especially in a system as structured as the US financial market. Many beginners feel overwhelmed because credit seems complex, but much of that confusion comes from not knowing how the system evaluates risk.

Credit functions as an access and cost system. It influences how institutions assess reliability, which can shape approvals, pricing, and financial flexibility. Rather than focusing on short-term score changes, it helps to view credit as a long-term reliability record.

As credit knowledge deepens, learning about inquiry types and how they appear on reports becomes the next step in understanding score movement. Exploring hard vs soft inquiry differences helps connect application activity to credit reporting behavior.

Credit growth is usually about steady patterns, not instant perfection.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.