Many people are surprised to learn that everyone begins their financial journey without a credit history. If you are wondering whether it is possible to build credit with no history, you are not alone. For beginners, the idea of starting from zero in the credit system can feel confusing.

In the United States, credit history develops only after certain financial activities are reported to credit bureaus. Before that happens, there may simply be no record of borrowing or credit usage in the system.

Understanding how credit history begins helps reduce the uncertainty around building credit for the first time. Once the credit reporting process starts recording activity, a credit profile gradually develops over time.

Why Starting With No Credit History Is Common

Starting without any credit history is a normal situation for many people. The credit reporting system only records activity after certain financial events occur, so everyone effectively begins with no credit data in the system.

Understanding this starting point helps beginners see that having no credit history is simply the first stage of building a credit profile.

📄 Many People Begin With No Credit File

A person may have no credit file if they have never used credit products that report activity to credit bureaus.

This may happen when someone has:

- Never opened a credit card

- Never taken a loan

- Not used financing services reported to credit bureaus

Without recorded activity, the credit system has no information to generate a credit report.

🧭 Credit History Must Start Somewhere

Credit history develops only after financial activity begins to appear in the reporting system. Once a credit account is opened and used, that activity can begin to create a credit record.

Over time, as more activity is reported, the credit file gradually grows and becomes more detailed.

The US Credit System Relies on Reported Activity

In the United States, credit bureaus build credit reports based on information provided by lenders and financial institutions.

These institutions report account activity, payments, and other credit-related data. Learning the difference between thin file vs no file helps explain how credit profiles evolve once the reporting system begins recording activity.

Starting with no credit history is normal because credit reports only develop after financial activity is reported.

How Credit History Actually Begins

Credit history does not appear automatically. It begins only when certain financial activities are reported to the credit bureaus. Once these activities are recorded, the credit reporting system starts building a credit profile over time.

Understanding how this process works helps beginners see how credit history gradually develops.

📄 Credit Accounts Create Records

The starting point for credit history is usually the creation of a credit account.

Examples may include:

- Opening a credit card account

- Taking a small loan

- Using financing services that report to credit bureaus

When these accounts are opened and used, they begin generating financial activity that can be tracked.

🏢 Reporting to Credit Bureaus

In the United States, lenders and financial institutions may report account activity to credit bureaus.

These reports may include:

- Account openings

- Payment activity

- Credit balances

- Account status

Once this information is reported, it becomes part of the credit reporting system.

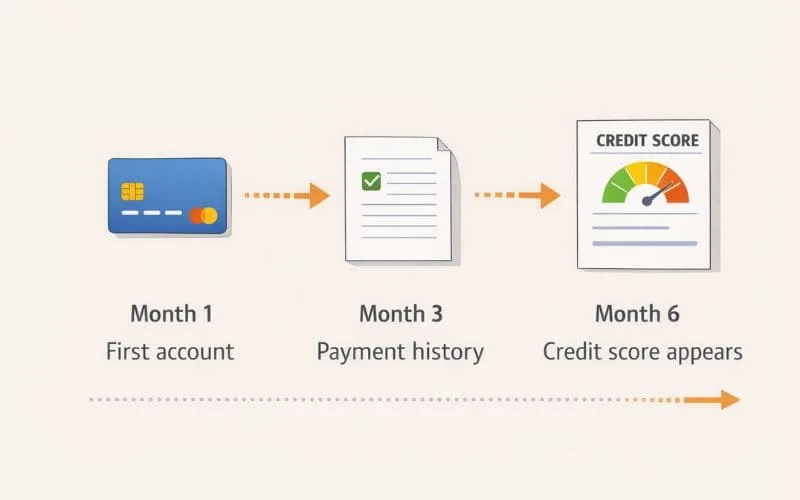

📊 First Activity Appears on Credit Reports

After financial activity is reported, the first entries begin to appear on a credit report. Over time, these records expand as more account history and payment information is added.

Because credit scores are calculated based on reported data, understanding how often credit scores update can help beginners see how these records gradually influence credit profiles.

Credit history begins when financial activity is reported to credit bureaus and recorded on a credit report.

Why Lenders Need Credit History

Credit history provides lenders with a record of how someone has managed financial responsibilities over time. Because lending involves risk, financial institutions rely on historical credit data to help evaluate applications.

Without credit history, lenders may have limited information available to understand how someone handles credit.

📊 Risk Evaluation

When lenders review an application, they often evaluate the level of financial risk involved.

Credit history can provide signals such as:

- How consistently payments are made

- How accounts are managed

- How credit has been used in the past

These signals help lenders estimate the likelihood of future repayment.

🔄 Borrowing Patterns

Credit reports also show patterns of credit behavior over time.

For example, lenders may observe:

- How often credit is used

- How accounts are maintained

- How long credit relationships last

These patterns help provide context beyond a single financial decision.

⚙ Credit Scoring Models

Credit scoring models use information from credit reports to generate credit scores.

These models evaluate several factors together to estimate financial reliability. Understanding why payment history matters helps beginners see how repayment behavior becomes an important part of the credit evaluation process.

Lenders rely on credit history to evaluate financial reliability and estimate future borrowing behavior.

Why Building Credit Takes Time

Building credit is not an instant process. Credit history develops gradually because the credit reporting system collects information over time. Lenders and scoring models rely on patterns of behavior rather than one-time financial activity.

Because of this, creating a stable credit profile usually requires consistent activity across multiple reporting periods.

⏱ Reporting Cycles

Credit information is not updated continuously in real time. Instead, financial institutions typically report account activity during scheduled reporting cycles.

These cycles allow credit bureaus to record information such as:

- Account balances

- Payment activity

- Account status

As these updates accumulate, the credit report gradually becomes more detailed.

📊 Behavior Patterns

Credit scoring systems evaluate patterns that develop over time rather than single events.

For example, scoring models may observe:

- Consistent payment behavior

- Ongoing account activity

- Responsible credit usage

Because these patterns require time to develop, credit history becomes more reliable as more data is recorded.

⚙ Credit Scoring Models

Credit scoring models analyze credit reports using historical data collected over time. The longer the record of financial activity, the more information these models have to evaluate credit behavior.

Understanding how long it takes to build credit from zero helps beginners see why building a credit profile usually happens gradually rather than instantly.

Credit systems rely on long-term patterns, which is why building credit typically takes time.

Common Beginner Misunderstandings About Starting Credit

When people first learn about credit history, several misunderstandings can create confusion. Many beginners assume that credit history works instantly or that having no credit automatically means having bad credit.

In reality, credit history develops gradually and is based on recorded financial activity over time.

❌ “Credit History Appears Instantly”

One common misunderstanding is that a credit history appears immediately after opening a credit account.

In practice, credit history develops only after activity is reported to credit bureaus and recorded on credit reports. This process may take time because lenders report information during scheduled reporting cycles.

Because of this delay, new credit activity may not appear instantly.

❌ “No Credit Means Bad Credit”

Another misconception is that having no credit history is the same as having poor credit.

In reality, these situations are different. Having no credit history simply means the credit reporting system does not yet have enough information to evaluate credit behavior.

Bad credit, on the other hand, usually refers to negative information recorded on a credit report.

❌ “You Need Debt to Start Credit”

Some beginners assume that building credit always requires taking on large amounts of debt.

However, credit history is primarily built through recorded credit activity and repayment behavior, not simply through borrowing large amounts. Understanding common beginner money mistakes can help explain why misconceptions about credit sometimes lead to unnecessary financial stress.

Many concerns about starting credit come from misunderstandings about how credit history actually develops.

What Happens After Credit History Starts

Once the first credit activity appears on a credit report, the credit reporting system begins building a financial profile. This process happens gradually as more information is recorded across time.

Each new entry on the credit report adds data that helps lenders and credit scoring models better understand credit behavior.

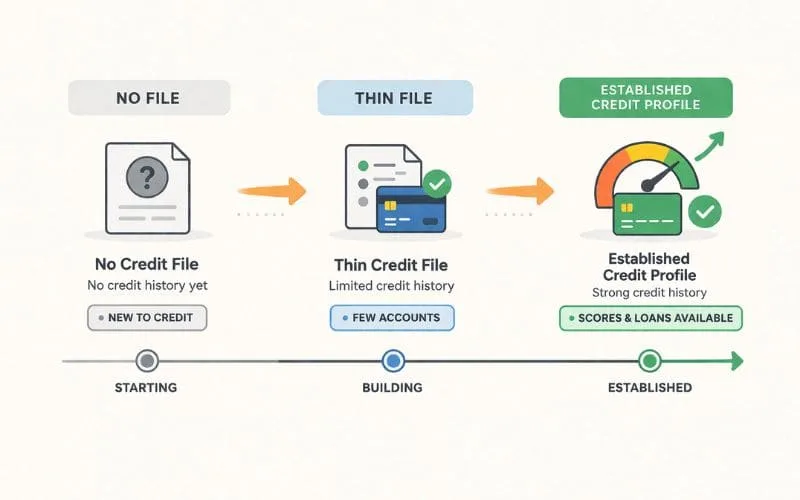

📄 Thin File Stage

At the beginning, most people enter what is commonly called the thin file stage. This means that the credit report contains only a small amount of information.

For example, the report may show:

- One or two credit accounts

- Limited payment history

- A short timeline of credit activity

Because there is limited data, credit scoring models may have less information available for evaluation.

📊 Score Generation

As activity continues to be reported, credit scoring systems may eventually generate a credit score. This score is calculated using the information recorded on the credit report.

The score reflects patterns such as:

- Repayment behavior

- Account management

- Credit usage activity

As the credit report grows, the score may change as new data is added.

📈 Credit Profile Growth

Over time, additional credit activity expands the credit profile. With more information available, lenders can better understand long-term credit behavior.

Factors such as credit utilization also begin playing a role in how credit scores are calculated once a credit history exists.

After credit history begins, the credit profile gradually grows as more financial activity is recorded.

How Beginners Should Think About Building Credit

For beginners, building credit can sometimes feel complicated or slow. However, credit systems are designed to evaluate behavior across time rather than short-term activity. Understanding this helps shift the focus from quick results to consistent financial patterns.

A long-term mindset makes the credit building process easier to understand.

📈 Long-Term Behavior

Credit reports are built from historical data that develops gradually. Each recorded activity adds another piece to the overall credit profile.

Over time, consistent patterns help create a clearer financial history.

⏳ Patience > Speed

Credit development rarely happens instantly. Because lenders and scoring models evaluate patterns across multiple reporting cycles, building a stronger credit profile often requires time.

Allowing credit history to grow gradually helps create a more stable credit record.

🔁 Consistency > Shortcuts

Credit scoring models tend to evaluate long-term reliability rather than short bursts of activity.

Consistent credit behavior across months and years usually provides stronger signals of financial stability.

👁 Awareness > Optimization

For beginners, understanding how the credit system works is often more valuable than trying to optimize every small detail.

Learning how credit scores affect financial life helps provide a broader perspective on how credit history connects to everyday financial opportunities.

Building credit is primarily about consistent behavior across time rather than quick short-term results.

FAQs

Can you build credit with no history?

Yes, it is possible to build credit with no history. Everyone begins the credit process without a credit record, and credit history develops only after financial activity is reported to credit bureaus.

Once a credit account is opened and used, the reporting system begins recording information such as account activity and payment behavior. Over time, these records form the foundation of a credit profile that lenders can review.

Because credit systems rely on historical data, the process of building credit gradually expands as more activity appears on a credit report.

How does credit history start?

Credit history usually begins when a financial account that reports to credit bureaus is opened and used. Examples may include credit cards, installment loans, or other credit-based accounts.

When lenders report account activity to credit bureaus, that information becomes part of the credit report. The first entries on a credit report typically include account details, payment activity, and account status.

As additional activity is reported over time, the credit report becomes more detailed and begins forming a complete credit history.

How long does it take to build credit?

Building credit typically takes time because credit scoring systems evaluate patterns of financial behavior across multiple reporting cycles.

The credit reporting system collects data gradually as lenders report account activity. Because of this process, credit history develops step by step rather than appearing instantly.

Over time, consistent credit activity can help create a more detailed credit profile, allowing lenders and scoring models to evaluate financial behavior more accurately.

Can you have a credit score with no history?

In most cases, a credit score cannot be generated without any recorded credit history. Credit scoring models require some amount of credit data before calculating a score.

Once credit activity appears on a credit report and enough information is available, a credit score may eventually be generated. The score reflects patterns of credit behavior recorded in the credit report.

This is why people who are just starting their credit journey may not see a score immediately.

Why do lenders require credit history?

Lenders use credit history to understand how someone has managed financial responsibilities in the past. Because lending involves financial risk, lenders often rely on historical credit data to evaluate reliability.

Credit reports provide information about account activity, payment patterns, and credit usage. These records help lenders estimate the likelihood that a borrower will manage credit responsibly in the future.

Without credit history, lenders may have limited information available for evaluating applications.

Does everyone start with no credit?

Yes, everyone begins without a credit history. The credit reporting system only records financial activity after certain credit-related events occur.

Until those activities are reported to credit bureaus, there may simply be no credit data associated with a person. Once credit accounts begin generating reported activity, the credit report gradually develops.

Over time, this recorded history becomes the foundation of a person’s credit profile.

Final Thoughts

Starting without any credit history is a completely normal part of the financial journey. Everyone who participates in the credit system begins at the same starting point, where no credit data has yet been recorded.

Credit building usually happens gradually as financial activity begins appearing on credit reports. As accounts are opened, used responsibly, and maintained across time, the credit reporting system collects more information and builds a clearer credit profile.

Understanding how this process works can remove much of the confusion that beginners often feel when learning about credit. Instead of expecting immediate results, it becomes easier to view credit development as a long-term process based on consistent financial behavior.

Exploring the pros and cons of side hustles can also help provide a broader perspective on how income flexibility and financial stability connect to overall financial health.

Every credit profile begins somewhere, and learning how the system works makes the journey much easier to navigate.

I’m Daniel Moore, the founder of SimpleMoneyLab, where I help beginners learn Personal Finance in a simple and realistic way. I focus on breaking down Budgeting, Credit Basics, and Side Hustles into plain English so everyday Americans can feel more confident with Money.