Building credit for the first time can feel confusing, especially in the United States where many everyday decisions involve credit checks. For beginners, one of the most common frustrations is opening a credit account and then realizing a credit score still doesn’t appear anywhere. It’s a confusing moment because nothing in the system tells you how long you’re supposed to wait or when a score will show up.

Part of that confusion comes from not knowing whether you’re starting with no credit file at all or a thin credit file with only limited information. In both cases, scoring models need time and reported activity before generating a score for the first time.

This guide explains how long it typically takes to build credit from zero in the U.S., why the delay is normal, and what beginners can realistically expect from the timeline.

What Does “Building Credit From Zero” Mean?

Building credit from zero means starting without any previous credit history in the U.S. system. Many beginners assume that having no debt automatically means they have good credit, but in reality the credit system needs recorded data before it can generate a score at all.

There are two common situations beginners fall into:

🆕 No Credit File — no information reported to credit bureaus yet

📂 Thin Credit File — some information exists, but not enough for scoring models to evaluate

This situation is especially common among:

👥 New graduates, young adults, and recent U.S. immigrants, who are interacting with credit for the first time.

Before a score can appear, credit bureaus must receive enough reported activity from lenders. Scoring models need this data to evaluate payment behavior and create a score for the first time.

When Does a Credit Score First Appear?

A credit score doesn’t appear as soon as someone opens a credit account. Scoring models need enough reported activity to evaluate how a person handles borrowed money, which takes time.

In the U.S., lenders send information to credit bureaus on periodic reporting cycles, often tied to billing statements. Because these reporting cycles vary, beginners may see credit activity on their statements long before a score appears anywhere.

This waiting period often causes confusion, especially for new grads, young adults, and recent immigrants who expect a score to show up immediately. In reality, scoring models can’t generate a score until they have enough data to work with — and that data has to be reported first.

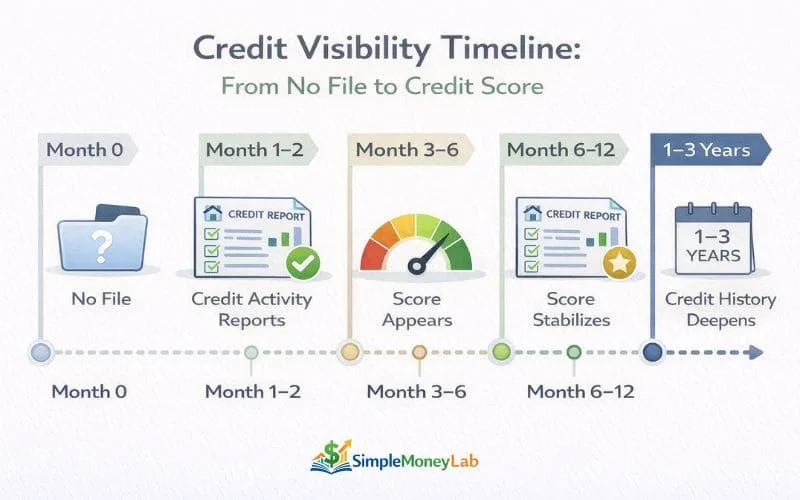

How Long Does It Take to Build Credit From Zero?

In the United States, it typically takes three to six months of reported credit activity for a credit score to appear for the first time. The timeline can vary based on reporting cycles and how quickly enough information becomes available.

Because the U.S. credit system depends on lender reporting, scoring models need to receive multiple months of data before they can evaluate credit behavior. This delay is normal, and many beginners experience a period where credit activity exists but no score is visible yet.

What Affects the Timeline?

Even though most beginners receive their first credit score within a few months, the timeline isn’t identical for everyone. Several factors influence how quickly scoring models have enough information to begin evaluating credit behavior.

🗓 Reporting Cycles

Most lenders report account activity to credit bureaus on monthly billing or statement cycles. Because these cycles vary across lenders, some information may appear sooner while other updates arrive later, creating natural delays in the scoring process.

💳 Account Types

Different account types contribute different kinds of information to a credit file. For example, revolving accounts (such as credit cards) and installment accounts (such as auto or student loans) report activity differently, which can affect how credit histories form in the early months.

📚 Credit Mix

Scoring models evaluate more than one type of credit over time. When someone only has a single account type, the informational depth in their file may develop more slowly compared to someone whose credit file includes multiple types of accounts.

📅 Payment History

Credit scoring relies on payment patterns rather than isolated transactions. Reporting systems need multiple payment cycles to understand consistency, which naturally requires time to accumulate.

🗂 Thin File vs. No File

Beginners with a thin file already have some credit information reported and may see a score appear sooner. Those with no file start entirely from scratch, which can lengthen the initial timeline because scoring models must wait for credit data to exist at all.

Once credit history begins forming, the next question becomes How Credit Scores affect your Financial life beyond borrowing.

How Credit Is Evaluated in the US

Credit in the United States is evaluated through a system built around reported financial behavior rather than self-declared information. When someone uses credit, lenders send account activity to credit bureaus, which store that information in a credit report. This creates the data foundation that scoring models rely on.

Scoring models then analyze that reported data to produce a credit score. The score summarizes credit behavior into a three-digit number that can be used by institutions to assess creditworthiness. The evaluation focuses on how someone has borrowed and repaid money, not on how much they earn.

Personal income, savings, and assets are not included in the credit reporting process. Unlike other financial systems where individuals self-report information, the U.S. credit system depends on third-party reporting and historical behavior over time.

Real-Life Scenarios for Beginners (US)

Many beginners learn about the U.S. credit system through real-life situations rather than formal explanations. These scenarios show how credit can begin from zero even when someone is actively using financial products.

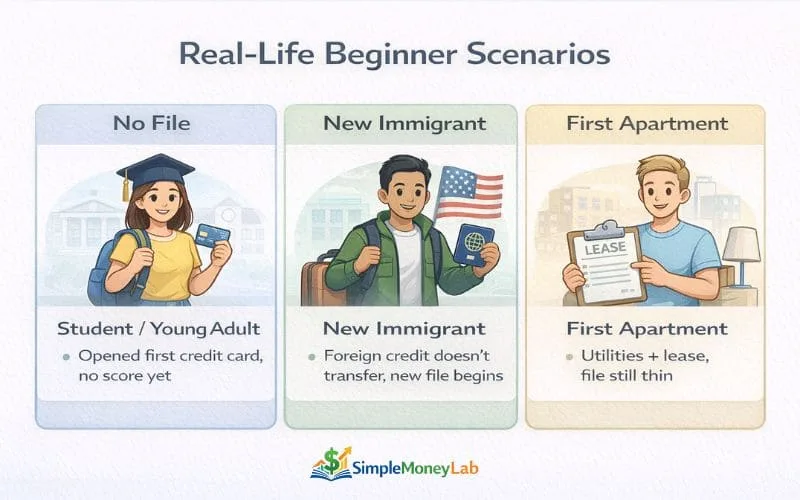

👩🎓 Student / Young Adult

A college student opens their first credit card and uses it for small purchases. Statements arrive and payments are made, but no credit score appears when they check. From their perspective, credit activity is happening — but scoring models are still waiting for enough reported cycles to generate a score for the first time.

🌎 New Immigrant

A recent immigrant moves to the U.S. with financial history from their home country. Even if they had loans, credit cards, or strong repayment habits abroad, that information doesn’t automatically transfer into the U.S. system. As a result, they begin with a new credit file and wait for reported activity to accumulate before a score becomes visible.

🧑💼 First Job / First Apartment

A young professional signs a lease, sets up utilities, or applies for a phone plan. These interactions may involve credit checks, but they don’t always generate enough reportable data to create a score right away. Credit activity has started, yet their file may remain “thin” until credit accounts begin reporting consistently.

Credit Score vs Credit History

Credit history and credit score are related, but they are not the same thing. Credit history refers to a record of how someone has used credit over time — including opened accounts, payment activity, and other reported information. It forms the timeline that scoring models evaluate.

A credit score, on the other hand, is a three-digit number generated from that history to summarize credit behavior in a standardized way. A score cannot exist without enough history for scoring models to analyze, which is why beginners often go through a phase where they have credit activity but no visible score yet.

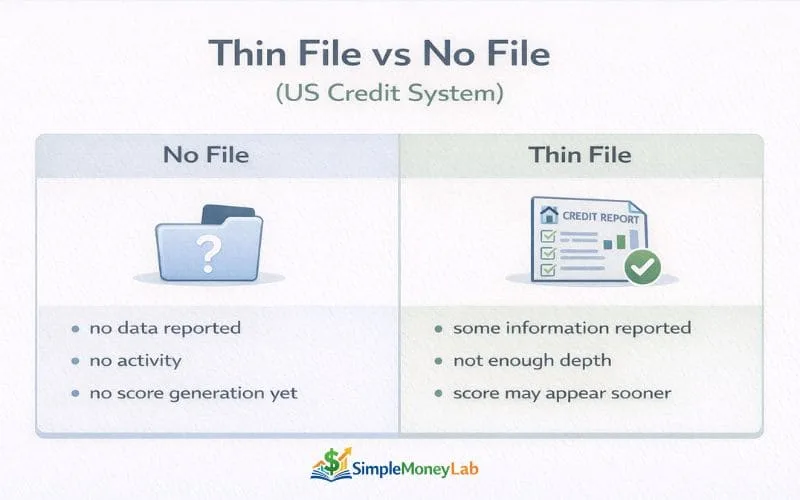

Thin File vs No File (Key Difference)

Beginners often hear the terms thin file and no file, and while they sound similar, they describe two different situations in the U.S. credit system.

A No file situation means nothing has been reported to the credit bureaus yet. There is no record of credit accounts, payment activity, or inquiries. In this case, scoring models have no data to analyze at all.

A Thin file means some information has been reported, but not enough for scoring models to generate a credit score. Thin-file beginners may already have a credit card or loan reporting, but the file still lacks the depth or history needed for scoring models to evaluate behavior.

Because of this distinction, thin-file consumers often receive a score sooner than no-file consumers once enough information accumulates over multiple reporting cycles.

Frequently Asked Questions

How long does it take to get a credit score from zero?

In the United States, many beginners receive their first credit score within three to six months of reported credit activity. The timeline varies because lenders report on different billing cycles, and scoring models need enough data before a score can be generated for the first time. A delay during the early months is common.

Can you build credit without a credit card?

It’s possible to begin building credit without a credit card, although many beginners start with one because it reports frequently. Other financial products that report to credit bureaus can also contribute to establishing a credit file, depending on how the lender reports information. The key requirement is the presence of reported credit activity.

Why does a credit score take months to appear?

Credit scoring models evaluate payment behavior and account history over time, which requires multiple reporting cycles to develop. Even if a beginner opens a credit account immediately, lenders may not report information until the end of the first billing period. This creates a waiting phase where activity exists but no score is visible yet.

Does income affect how fast I build credit?

Personal income does not appear on credit reports and is not used directly by scoring models to generate a credit score. Credit scoring focuses on reported credit behavior rather than financial capacity or earnings. As a result, higher income does not automatically accelerate the timeline for receiving a credit score.

Can immigrants build credit in the US?

Yes, immigrants can build credit in the U.S., although prior credit history from other countries typically does not transfer. Most newcomers begin with either a thin credit file or no file at all and wait for reported information to accumulate before a score becomes visible. This process follows the same reporting rules as it does for U.S. beginners.

Final Thoughts

Building credit from zero takes time, and it’s normal for beginners in the U.S. to go through a period where credit activity exists but no score appears yet. The delay isn’t a sign that something is wrong — it reflects how the credit reporting and scoring systems are designed to evaluate consistent behavior over multiple cycles.

Understanding this timeline can make the early stages of credit less confusing. A score doesn’t appear instantly, and it doesn’t reflect someone’s income, savings, or financial potential. It simply summarizes reported credit behavior once enough information becomes available.

For many beginners, the journey from no file to a visible score is the first step toward participating in the broader U.S. credit system. In that context, progress matters more than speed, and clarity makes the process feel less uncertain.