Many US beginners feel confused when they first start using credit cards, especially when credit limits and balances don’t always seem easy to understand. A common misunderstanding is thinking that a credit limit automatically represents safe spending power, when in reality, credit usage is evaluated very differently inside the credit system.

Understanding what is credit utilization helps explain how credit card usage is measured and why it plays a role in credit score behavior. Credit utilization shows how much of available credit is being used at a given time, which helps lenders evaluate financial risk patterns.

Because the US financial system relies heavily on credit scoring for approvals, pricing, and access, learning how credit usage is measured can help beginners better understand how everyday credit behavior connects to long-term financial flexibility.

Why Credit Utilization Matters in Real Life

In real life, credit cards are not only payment tools — they are also behavior signals inside the US credit system. Many beginners focus only on paying bills on time, but credit usage patterns are also part of how credit risk is evaluated.

For many people, credit stress happens when balances grow close to limits, even if payments are still being made. This happens because credit scoring systems evaluate how much credit is being used, not just whether payments are made.

💳 Credit Card Usage vs Credit Limits

Credit utilization measures how much of available credit is being used at a given time.

In practical terms, this compares:

- Current Credit Card balance

- Total Available Credit limit

Using a large portion of available credit can sometimes signal higher risk patterns to lenders, even if payments are current.

📊 Credit Score Impact Behavior

Credit utilization is one of the signals used to understand credit behavior patterns.

Credit scoring models often evaluate:

- How often balances stay high

- How much credit is used compared to limits

- Whether usage patterns change frequently

This is why two people with the same payment history can still have different credit score outcomes.

Credit utilization is calculated using reported balances, which means timing matters. Learning how often do credit scores update helps clarify why utilization changes may not appear immediately after a payment is made.

🏦 Access and Approval Connection

Credit utilization can sometimes influence access to financial products.

In real life, credit patterns can connect to:

- Loan approvals

- Credit line increases

- Interest rate offers

- Deposit requirements

Lenders often evaluate risk patterns using credit behavior data, not just payment history alone.

US Credit Reliance System

The US financial system relies heavily on credit scoring for many everyday approvals.

Credit behavior can affect areas like:

- Housing applications

- Insurance pricing models

- Financing approvals

- Service deposit requirements

Because credit scoring is widely used, credit utilization becomes part of broader financial access patterns.

Credit utilization matters because it shows how credit is used in real life — not just whether payments are made.

What Is Credit Utilization?

For many beginners, credit card limits can feel like spending limits, but credit systems evaluate usage differently. Credit utilization is not about how much credit is available — it is about how much of that credit is currently being used.

Understanding what is credit utilization means understanding how lenders measure credit card usage compared to total available credit. Credit utilization is usually expressed as a percentage that compares total credit card balances to total credit limits.

Credit utilization helps show how actively credit is being used at a given time.

🧾 Real-Life Meaning

In real life, credit utilization reflects how much credit is being relied on during everyday spending.

For example, utilization changes when:

- Balances increase

- Balances decrease

- Limits change

- Multiple cards are used together

Credit behavior is evaluated over time, not just at one moment.

Understanding how credit behavior connects to financial life helps explain why credit usage patterns matter. Learning how credit patterns influence approvals and access is part of understanding How Credit affects Everyday Financial life.

🚫 Credit Utilization ≠ Spending Ability

One of the most common beginner misunderstandings is assuming credit limits represent safe spending power.

In reality:

- Credit limit = Maximum available credit

- Credit utilization = How much of that credit is currently used

Using a large portion of available credit can sometimes signal higher borrowing reliance, even if payments are made on time.

Credit utilization is commonly defined as the percentage of available credit that is currently being used. For example, if someone has a total credit limit and uses a portion of that credit, utilization reflects how much of that borrowing capacity is being used at a given time. According to Consumer Credit Research and Industry data, credit utilization is calculated by comparing credit card balances to total available credit limits.

Credit utilization measures credit usage patterns — not spending permission.

How Credit Utilization Works in the US Credit System

In the United States, credit behavior is tracked through reporting systems that update credit activity regularly. Credit utilization is not calculated manually by borrowers — it is calculated automatically based on reported credit card balances and available credit limits.

For many beginners, credit utilization can feel confusing because it changes as balances and limits change, even if no new purchases are made.

💳 Credit Limit Concept

A credit limit is the maximum amount that can be borrowed on a credit card account.

Credit limits are set based on factors such as:

- Credit history

- Income indicators

- Past borrowing behavior

- Lender risk models

Credit limits define available credit capacity, which is used to calculate utilization.

📊 Balance vs Limit Ratio

Credit utilization is calculated by comparing total balances to total available credit limits.

This ratio helps show:

- How much credit is currently being used

- How often credit balances stay high

- How credit usage patterns change over time

Utilization is usually expressed as a percentage.

📅 Monthly Reporting Behavior

Credit card activity is typically reported to credit bureaus on regular reporting cycles.

This means:

- Utilization can change monthly

- Balances at reporting time matter

- Credit scores reflect reported patterns over time

Because reporting happens in cycles, utilization is not fixed — it changes with credit activity.

🏦 Lender Risk Interpretation

Lenders often use credit utilization as one signal of borrowing behavior patterns.

Utilization can help show:

- Borrowing reliance patterns

- Credit usage consistency

- Credit exposure levels

Credit utilization is usually evaluated together with payment history and other credit factors.

Credit utilization works as a real-time signal of credit usage behavior inside the US credit reporting system.

Why Credit Utilization Affects Credit Scores

Credit scores are designed to predict how credit is likely to be used over time, not just whether payments are made. Because of this, credit scoring models look at multiple behavior signals, and credit utilization is one of the indicators used to understand borrowing patterns.

For many beginners, it can feel confusing that credit scores can change even when payments are made on time. This happens because credit scores measure overall credit behavior, not just payment history alone.

📉 Risk Signal Logic

Credit utilization helps act as a risk signal inside credit scoring models.

Higher utilization can sometimes suggest:

- Higher reliance on borrowed money

- Reduced available credit cushion

- Potential short-term borrowing pressure

Lower utilization can sometimes signal more available credit flexibility.

👀 Borrowing Pattern Visibility

Credit utilization helps show borrowing patterns over time, not just at one moment.

Credit scoring models may evaluate:

- How often balances stay high

- How quickly balances change

- How consistently credit is used

Credit scoring focuses on patterns, not single events.

🧾 Payment Behavior Context

Payment history remains very important, but credit utilization adds context to payment behavior.

For example:

- On-time payments + high utilization = Heavy credit reliance pattern

- On-time payments + lower utilization = Lower exposure pattern

Understanding how credit factors work together helps explain overall credit score behavior. Learning How Credit Scores work helps beginners understand how utilization fits into the full credit scoring system.

Credit utilization affects credit scores because it helps show how credit is used, not just whether it is paid on time.

Common Credit Utilization Mistakes Beginners Make

Many credit utilization mistakes happen because credit limits and balances are easy to misunderstand at the beginning. For many US beginners, credit cards feel like flexible payment tools, but credit systems evaluate how credit is used over time, not just how payments are made.

Most utilization mistakes happen because of visibility gaps rather than poor financial discipline.

⚠️ Using Full Credit Limits

Some beginners assume that using most or all of a credit limit is normal as long as payments are made.

In real life, high balance usage can sometimes signal:

- Heavy credit reliance

- Lower available credit cushion

- Higher borrowing exposure patterns

Utilization is based on how much credit is used, not just whether payments are current.

💳 Thinking Credit Limit = Spending Power

Credit limits show the maximum available borrowing capacity, not recommended spending levels.

Common misunderstanding patterns include:

- Treating credit limit like extra income

- Assuming full limit usage has no credit impact

- Confusing borrowing capacity with spending comfort

Credit limits define borrowing space, not spending safety.

📅 Ignoring Statement Timing

Credit utilization is often based on reported balances, not just payments made later.

This means:

- Balances at reporting time matter

- Utilization can change monthly

- Scores can move even when payments are on time

Reporting timing plays a role in how utilization appears in credit data.

🔁 Carrying High Balance Cycles

Consistently carrying higher balances over multiple cycles can create visible borrowing patterns.

Over time, this can reflect:

- Repeated high utilization patterns

- Reduced available credit flexibility

- Higher overall credit exposure signals

Understanding broader money behavior patterns helps explain why credit habits develop over time. Learning about Common Beginner Money Mistakes helps show how credit behavior fits into overall financial behavior patterns.

Most credit utilization mistakes come from misunderstanding how credit is measured, not from intentional misuse.

Credit Utilization vs Credit Limit vs Credit Balance

Many beginners hear these three terms together and assume they mean the same thing. In real life, Credit utilization, Credit limit, and Credit balance each represent different parts of how credit accounts work. Understanding how these three connect helps make credit reports and credit behavior easier to interpret.

Credit systems evaluate how these three numbers interact, not just each number individually.

📊 Credit Utilization vs Credit Limit

A credit limit is the total amount of credit available on an account. Credit utilization shows how much of that available credit is currently being used.

In simple terms:

- Credit limit = Maximum borrowing capacity

- Credit utilization = Percentage of limit currently used

Credit limits define borrowing space, while utilization shows borrowing activity.

💳 Credit Utilization vs Credit Balance

A credit balance is the total amount currently owed on a credit account. Credit utilization compares that balance to the total available credit limit.

In practical terms:

- Balance = Amount currently owed

- Utilization = Balance ÷ Limit (expressed as percentage)

Utilization turns balance data into behavior pattern data.

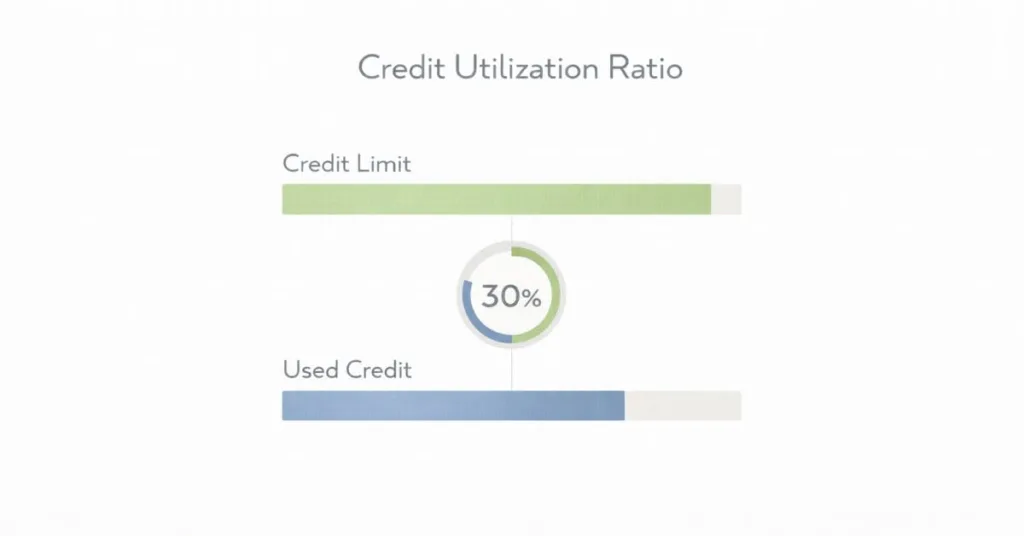

Example Scenario:

Credit limit = $1,000

Balance = $300

Credit utilization = 30%

If the balance increases or limit changes, utilization changes automatically.

This is why utilization can move even when spending habits feel similar — because utilization depends on both balance and limit together.

Credit limit shows borrowing capacity, credit balance shows what is owed, and credit utilization shows how much credit is being used relative to available limits.

US-Specific Credit System Factors

In the United States, credit behavior is tracked through reporting and scoring systems that continuously evaluate credit activity. Credit utilization is not viewed in isolation — it is interpreted within broader credit reporting cycles and credit scoring models.

For many beginners, credit behavior can feel confusing because credit scores respond to patterns over time, not just single transactions or payments.

📅 Monthly Reporting Cycles

Credit card activity is typically reported to credit bureaus on regular reporting schedules.

This means:

- Balances at reporting time are recorded

- Utilization can change monthly

- Credit scores reflect reported patterns over time

Because reporting happens in cycles, utilization is dynamic rather than fixed.

💳 Multi Card Usage Behavior

Many US consumers use more than one credit card at the same time.

Credit systems often evaluate:

- Total balances across all cards

- Total available credit across all accounts

- Combined utilization patterns

This is why overall credit usage patterns matter, not just single card activity.

📊 Credit Score Model Behavior

Credit scoring models evaluate credit behavior using multiple data signals.

Utilization is usually considered alongside:

- Payment history

- Account age

- Credit mix

- New credit activity

Utilization helps provide context to overall credit behavior.

🏦 Lender Evaluation Systems

Lenders often evaluate credit data using internal risk models in addition to credit scores.

These evaluations may consider:

- Credit usage consistency

- Credit exposure levels

- Historical borrowing patterns

Credit utilization helps lenders understand how available credit is used over time.

In the US credit system, credit utilization is evaluated as part of broader reporting cycles, scoring models, and lender risk assessments.

How Beginners Can Think About Credit Utilization

For many beginners, credit utilization can feel like a technical number that is difficult to control perfectly. In real life, credit behavior usually develops through patterns over time rather than through single monthly actions. Understanding how credit is used consistently often matters more than trying to manage credit activity perfectly in one billing cycle.

Credit systems are designed to evaluate long-term behavior patterns, not short-term perfection.

👀 Visibility > Perfection

Credit awareness usually matters more than trying to maintain perfect credit behavior every month.

- Understanding balance movement

- Noticing usage patterns

- Recognizing reporting timing effects

Credit systems evaluate patterns over time, not single perfect moments.

📊 Pattern > Single Month

Credit scoring models usually respond to long-term credit behavior patterns.

- One month rarely defines long-term credit behavior

- Consistent usage patterns are more visible

- Long-term behavior signals are stronger than short-term changes

Credit scoring is designed to evaluate trends rather than isolated events.

🔁 Consistency > Intensity

Stable, consistent credit behavior often matters more than large short-term changes.

- Consistent usage patterns create stable signals

- Sudden usage spikes create changing patterns

- Steady behavior is easier for systems to interpret

Credit systems usually reward predictable behavior patterns over time.

🧠 Understanding > Optimization

For beginners, understanding how credit systems work usually matters more than trying to optimize numbers quickly.

- System knowledge improves long-term decisions

- Awareness improves credit behavior confidence

- Learning reduces financial stress around credit usage

Learning how credit develops over time helps beginners understand realistic credit timelines. Exploring how long it takes to build credit from zero helps connect utilization behavior to long-term credit development patterns.

Credit utilization is best understood as a long-term behavior pattern, not a short-term number to control perfectly.

FAQs

What is credit utilization in simple terms?

Credit utilization is the percentage of available credit that is currently being used on credit cards. It compares total credit card balances to total credit limits to show how much credit is being used at a given time.

In simple terms, credit utilization helps show credit usage patterns rather than just credit availability. Credit systems use this information to understand how credit is being used over time.

Why does credit utilization matter?

Credit utilization matters because it is one of the behavior signals used to evaluate credit usage patterns. It helps credit scoring systems and lenders understand how much credit is being relied on compared to how much credit is available.

Credit utilization can influence how credit behavior is interpreted, especially when combined with payment history and other credit factors.

Does utilization affect credit score?

Yes, credit utilization can influence credit score calculations because it reflects credit usage behavior. Credit scoring models often evaluate utilization alongside other factors such as payment history, account age, and credit mix.

Utilization helps provide context about borrowing patterns rather than acting as a single standalone score factor.

Is high utilization bad?

High credit utilization can sometimes be interpreted as higher credit reliance, but credit scoring models usually evaluate utilization patterns over time rather than single moments.

Credit systems look at trends and consistency rather than only one reporting period.

How often does credit utilization change?

Credit utilization can change whenever credit card balances or credit limits change. It is often updated based on reporting cycles, which usually happen on a recurring schedule depending on the credit account and reporting timing.

Because of this, utilization is considered dynamic rather than fixed.

Does paying a credit card reduce credit utilization?

Paying down a credit card balance can reduce credit utilization because utilization is based on current balances compared to available credit limits. When balances decrease, utilization percentages typically decrease as well.

However, utilization patterns are usually evaluated over time rather than based on one single balance change.

Final Thoughts

Learning how credit works usually takes time, especially for beginners who are seeing credit reports, balances, and limits for the first time. Credit systems are built around long-term behavior patterns, which means understanding how credit is measured is part of the learning process, not something most people know immediately.

Credit utilization is not just a number — it is part of a larger credit behavior system. Over time, understanding how credit is used, how balances change, and how reporting works can help make credit activity feel more predictable and less confusing.

Credit health is often built through visibility and behavior awareness rather than short-term changes. As credit knowledge grows, many beginners naturally start exploring how other credit factors work together inside the credit system.

Understanding how payment history affects credit behavior is often the next step in learning how credit scores are built and how long-term credit patterns develop.

Credit is not about perfection — it is about learning how the system works over time.